Question

(a) Under the International Financial Reporting Standards, IAS 2 deals with inventories. Define the following terms:

i. Inventories (4 marks)

ii. Net Realisable Value (2 marks)

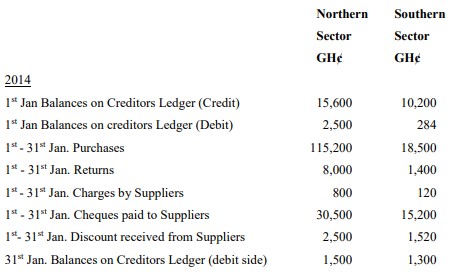

(b) Alpha Ltd. controls its Creditors’ Accounts by preparing monthly Creditors’ ledger Control Account in two parts, Northern and Southern Sectors.

The following figures were available as at January 31st 2014, when there was a difference of GH¢3,000 on the Trial Balance:

On 31st January, 2014, the officer in charge of the Northern Sector Ledger declared GH¢89,600, while that of the Southern Sector declared GH¢15,016.

You are required to:

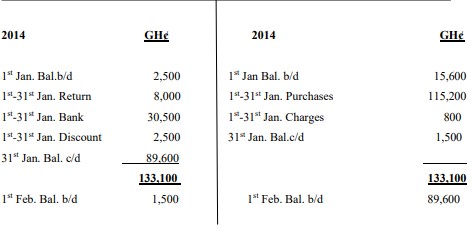

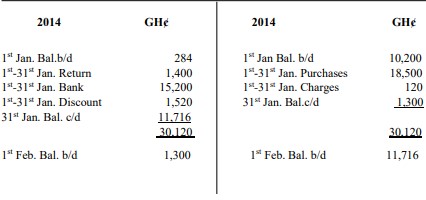

i. Prepare Creditors Ledger Control Account for the Northern and Southern Sectors, respectively. (12 marks)

ii. Draw any conclusion you can from the two Control Accounts. (2 marks)

Answer

(a)

i. Inventories are assets that are:

- Held for sale in the ordinary course of business.

- In the process of production for such sale.

- In the form of materials or supplies to be consumed in the production process or in the rendering of services.

- Goods purchased and held for resale e.g., goods held for sale by a retailer, or land and buildings held for resale.

- Finished goods produced.

- Raw materials.

- Work-in-progress.

ii. Net Realisable Value is the estimated selling price in the ordinary course of business, less the estimated cost of completion and the estimated cost necessary to make the sale.

(b) i. Northern Sector

Creditors Ledger Control Account

ii. Southern Sector

Creditors Ledger Control Account

ii. Conclusion:

The Control Accounts reveal that there is a difference of GH¢3,300 between the Control Account for the Southern sector (GH¢15,016 – GH¢11,716), which is the total discovered by the officer in charge of the Southern Sector. The Northern Sector ledger appears correct; however, the Southern Sector ledger should be rechecked for discrepancies.