Question

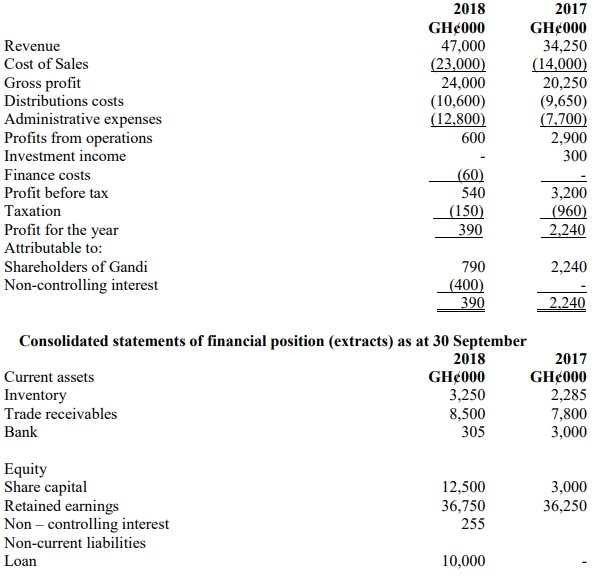

The Gandi Group (TGG) operates in the farming industry and has operated a number of 100% owned subsidiaries for many years. The Gandi group has its operations in the Brong-Ahafo Region of Ghana. Its financial statements for the last two years are shown below.

Additional Information:

- TGG has become increasingly worried about two major areas in its business environment: reliance on large supermarkets (which demand long payment terms), and the increase in fuel prices, which raises the cost of distribution.

- To address these concerns, TGG purchased 80% of Asida Ltd on 1 October 2017. This was TGG’s first acquisition of a subsidiary without owning 100% of it. Asida Ltd operates two luxury hotels in the Ashanti Region.

- TGG raised finance by disposing of GH¢5.5 million in investments (with a GH¢2.25 million gain on disposal, included in administrative expenses) and by taking a GH¢10 million loan.

- Asida Ltd opened a third hotel in Accra in March 2018. Initial reviews were poor, but feedback improved after the appointment of a new marketing director in May 2018.

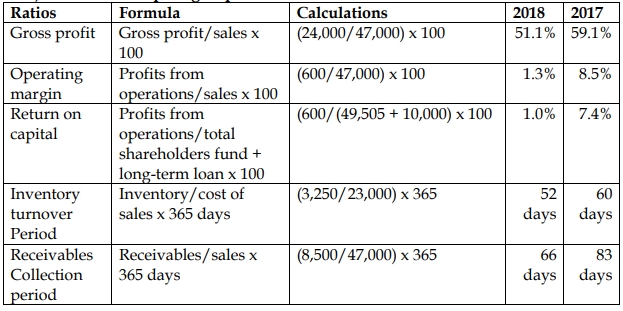

- Ratios for the year ended 30 September 2017:

- Gross profit margin: 59.1%

- Operating margin: 8.5%

- Return on capital employed: 7.4%

- Inventory turnover period: 60 days

- Receivables collection period: 83 days

Required: a) Prepare the equivalent ratios for the year ended 30 September 2018.

(5 marks)

b) Analyze the financial performance and cash flow of TGG for the year ended 30 September 2018, making specific reference to any concerns or expectations regarding future periods.

(10 marks)

Answer

a) Calculation of Ratios for the Year Ended 30 September 2018:

b) Analysis of Financial Performance and Cash Flow:

- Revenue and Profit Margins:

- TGG’s revenue has increased significantly by 37.2% from GH¢34,250,000 in 2017 to GH¢47,000,000 in 2018. However, this increase has not translated into a proportionate increase in profit, as the gross profit margin has fallen from 59.1% to 51.1%. This could indicate increased costs, particularly in distribution and administrative expenses, which have grown significantly.

- Operating Profit and Margins:

- The operating margin has dropped drastically from 8.5% in 2017 to 1.3% in 2018, despite the rise in revenue. This is a concerning sign, as TGG is barely profitable from its core operations. Part of this decline can be attributed to the GH¢2.25 million gain on disposal included in administrative expenses. Without this gain, TGG would have reported an operating loss.

- The poor performance of Asida Ltd may be contributing to these lower margins, as the new hotel in Accra only opened in March 2018 and has faced challenges with initial reviews.

- Return on Capital Employed (ROCE):

- TGG’s ROCE has decreased from 7.4% in 2017 to 1.0% in 2018, reflecting the declining profitability. The acquisition of Asida Ltd, while increasing revenue, seems to have diluted the overall return on the capital employed.

- Cash Flow Concerns:

- TGG’s cash position has deteriorated, with the bank balance falling to GH¢305,000. This is despite raising funds through a GH¢5.5 million investment disposal and a GH¢10 million loan. It appears that much of the cash has been absorbed by the acquisition of Asida Ltd and the associated costs of setting up the new hotel in Accra.

- The reduction in inventory turnover from 60 days to 52 days is a positive sign, indicating more efficient management of inventory.

- The receivables collection period has improved from 83 days to 66 days, which is beneficial for cash flow. However, reliance on supermarkets, as noted in the additional information, poses a risk to cash flow due to long payment terms demanded by them.

- Non-controlling Interest and Future Outlook:

- The non-controlling interest share of profit is negative (GH¢400,000), indicating that Asida Ltd is loss-making. This could be due to the challenges faced by the newly opened hotel in Accra. However, with improvements in feedback after the new marketing director’s appointment, there is hope for better performance in the future.

- The high fuel costs and reliance on supermarkets could continue to affect the profitability of TGG’s core farming operations.

Conclusion:

- TGG has experienced significant revenue growth, primarily due to the acquisition of Asida Ltd, but profitability has deteriorated. The company’s margins and return on capital have decreased, and its cash flow is under pressure despite raising funds. While there are positive signs of improvement at Asida Ltd, TGG’s reliance on supermarkets and rising costs, particularly in fuel, remain areas of concern for future periods.