Question

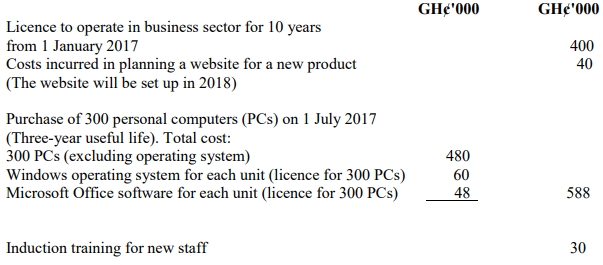

Nyame Ltd incurred the following expenditure during the year:

The company’s policy is to use the revaluation model for its intangible assets where a market valuation is available and permitted.

Required:

Recommend with suitable calculations the carrying amount of intangible assets at the end of the year 31 December 2017 according to the guidance given in IAS 38: Intangible Assets.

(5 marks)

Answer

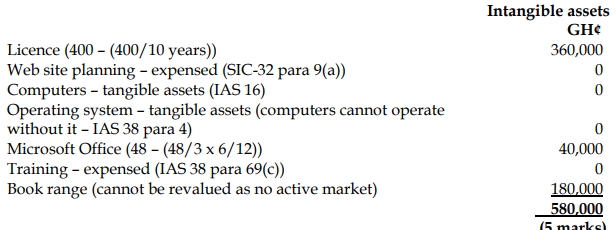

- License to Operate:

- The license is an intangible asset with a finite useful life of 10 years. The amortization for one year is calculated as:

- Amortization = GH¢400,000 ÷ 10 years = GH¢40,000.

- Carrying amount at 31 December 2017:

- GH¢400,000 – GH¢40,000 = GH¢360,000.

- The license is an intangible asset with a finite useful life of 10 years. The amortization for one year is calculated as:

- Website Planning Costs:

- According to IAS 38, costs incurred in the planning phase of website development should be expensed as incurred. Therefore, these costs are not capitalized.

- Carrying amount: GH¢0.

- Personal Computers and Software:

- The PCs are tangible assets and are not covered by IAS 38. The operating system (Windows) is essential for the PCs to function and should be classified as part of the tangible asset (PCs).

- Microsoft Office Software: This is an intangible asset with a 3-year useful life.

- Amortization for 6 months (since purchase was on 1 July 2017):

- Amortization = GH¢48,000 ÷ 3 years × 6/12 = GH¢8,000.

- Carrying amount at 31 December 2017:

- GH¢48,000 – GH¢8,000 = GH¢40,000.

- Induction Training:

- Under IAS 38, training costs are expensed as incurred and should not be capitalized.

- Carrying amount: GH¢0.

- Rights to Popular Books:

- The rights were initially purchased for GH¢180,000. At year-end, the rights were revalued to GH¢180,000 based on a market valuation. Since Nyame Ltd uses the revaluation model, the carrying amount at 31 December 2017 will be the revalued amount.

- Carrying amount at 31 December 2017: GH¢180,000.