Question

Answer

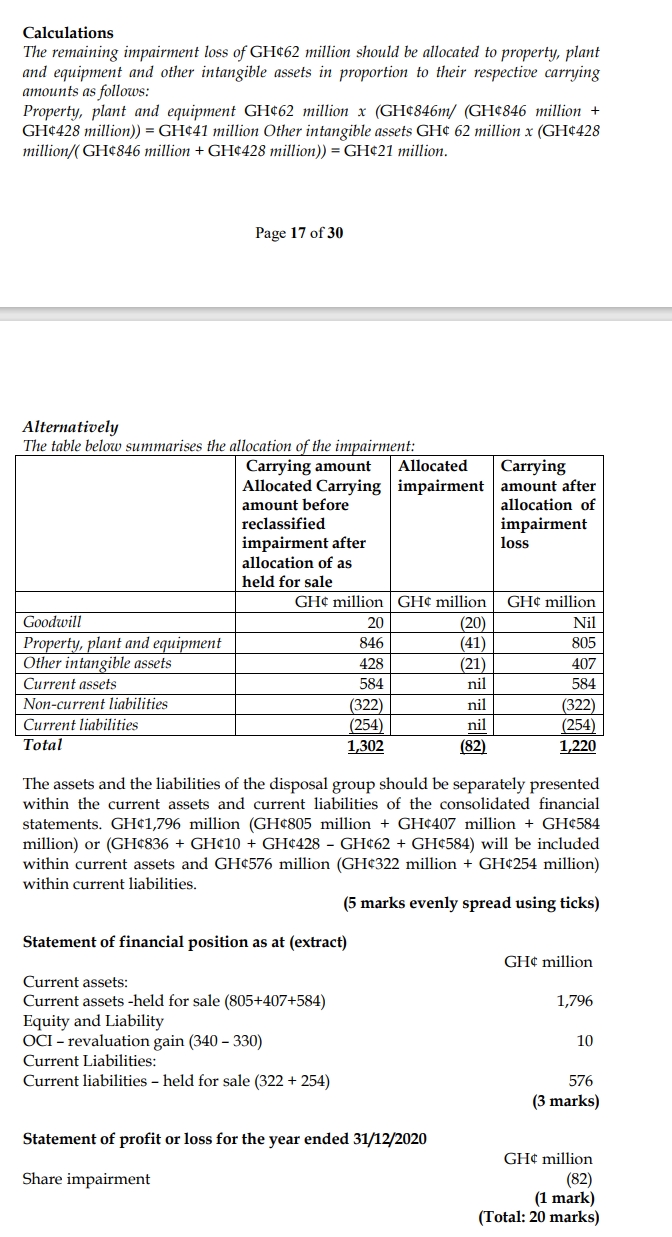

The goodwill in Jamila Ltd would originally be calculated as GH¢20 million (GH¢1,250 million – GH¢1,230 million). The net assets in Jamila Ltd are now GH¢1,292 million at 31 December 2020 (GH¢1,272 million per question and GH¢20 million goodwill). Since the group has a revaluation policy under IAS 16 Property, Plant, and Equipment, the group must revalue the property, plant, and equipment of Jamila Ltd to a fair value of GH¢340 million on classification as held for sale. A gain of GH¢10 million (GH¢340 million – GH¢330 million) would be recorded within other components of equity.

The net assets of Jamila Ltd would now have a carrying amount of GH¢1,302 million including GH¢846 million for property, plant, and equipment. On classification as held for sale, Jamila Ltd must be measured at the lower of the carrying amount and fair value less costs to sell. An impairment arises of GH¢82 million (GH¢1,302 million – GH¢1,220 million). This will first be allocated to the goodwill of GH¢20 million. The remaining impairment of GH¢62 million is allocated to non-current assets to which the measurement requirements of IFRS 5 apply. No impairment will therefore be allocated to the current assets of Jamila Ltd.