Question

Answer

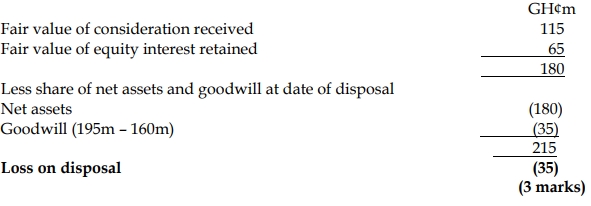

Afoko Ltd

Commentary/Justification:

After the disposal of 60% of equity, Afoko Ltd retains significant influence over Anyidohu Ltd. As a result, Anyidohu becomes an associate, and Afoko Ltd should account for the remaining investment using the equity method. Under the equity method, the investment is initially measured at the fair value of the retained equity interest (GH¢65 million). The group’s share of subsequent profits, comprehensive income, or losses of Anyidohu will be recognized in the group’s financial statements and will increase or decrease the carrying amount of the investment.