Question

Answer

1. Allocation of Head Office Assets to CGUs

The assets of the head office must first be allocated to the CGUs (Unit X, Unit Y, and Unit Z) based on the amounts provided:

| Unit | Carrying Value | Head Office Allocation | Total Carrying Value |

|---|---|---|---|

| Unit X | 500 | 95 | 595 |

| Unit Y | 700 | 280 | 980 |

| Unit Z | 1,000 | 375 | 1,375 |

2. Calculation of Impairment Loss

Next, compare the total carrying value of each CGU with its recoverable amount to determine if an impairment loss should be recognized.

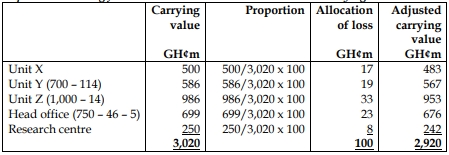

3. Allocation of Impairment Loss to Head Office and Other Assets

Impairment losses are allocated proportionately to the head office assets and other assets in each CGU:

4. Impairment Testing for Sikaman Plc as a Whole

Since the research facility cannot be allocated to the CGUs, an impairment test is conducted on the entity as a whole. The total assets after impairment losses are:

Note: Allocation loss = 3,020 – 2,920 = 100