i) Operating profit margin = Operating profit / Revenue x 100

- Atiku Ltd:

Operating profit = Net Profit + Finance cost + Tax provisions (Current tax + Deferred tax – Under-provision)

= 1,500 + 1,050 + 1,004 – 116

= 3,438

Operating profit margin = (3,438 / 25,600) x 100 = 13.43%

- Obi Ltd:

Operating profit = Net Profit + Finance cost + Tax provisions (Current tax + Deferred tax + Under-provision)

= 1,260 + 880 + 925 + 32 – 55

= 3,042

Operating profit margin = (3,042 / 21,900) x 100 = 13.89%

(1.5 marks)

ii) Return on Capital Employed (ROCE) = Operating profit / Capital employed x 100

- Atiku Ltd:

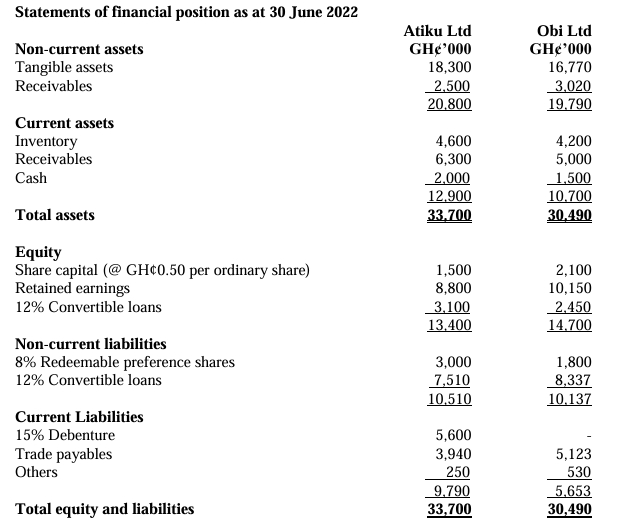

Capital employed = Equity + Non-current liabilities + Current liabilities related to interest-bearing liabilities (Debenture)

= 13,400 + 10,510 + 5,600

= 29,510

ROCE = (3,438 / 29,510) x 100 = 11.65%

- Obi Ltd:

Capital employed = Equity + Non-current liabilities

= 14,700 + 10,137

= 24,837

ROCE = (3,042 / 24,837) x 100 = 12.24%

(1.5 marks)

iii) Inventory turnover period = (Inventory / Cost of sales) x 365

Cost of sales for Atiku Ltd = Revenue – Gross profit = 25,600 x (100% – 22%) = 19,968

Cost of sales for Obi Ltd = Revenue – Gross profit = 21,900 x (100% – 25%) = 16,425

- Atiku Ltd:

Inventory turnover period = (4,600 / 19,968) x 365 = 84 days

- Obi Ltd:

Inventory turnover period = (4,200 / 16,425) x 365 = 93 days

(1.5 marks)

iv) Current ratio = Current assets / Current liabilities

- Atiku Ltd:

Current ratio = 12,900 / 9,790 = 1.32:1

- Obi Ltd:

Current ratio = 10,700 / 5,653 = 1.89:1

(1.5 marks)

v) Capital (long-term) gearing = Non-current liabilities / (Non-current liabilities + Equity) x 100

- Atiku Ltd:

Capital gearing = 10,510 / (10,510 + 13,400) x 100 = 43.96%

- Obi Ltd:

Capital gearing = 10,137 / (10,137 + 14,700) x 100 = 40.81%

(1.5 marks)

vi) Dividend yield = Dividend per share / Share price x 100

Dividend per share is calculated using the dividend coverage ratio:

- Atiku Ltd dividend per share = Earnings per share / Dividend coverage = (Net profit / Number of shares) / Dividend coverage

= (1,500 / 3,000) / 4 = 0.125

Dividend yield = (0.125 / 2.10) x 100 = 5.95%

- Obi Ltd dividend per share = Earnings per share / Dividend coverage = (1,260 / 4,200) / 5 = 0.06

Dividend yield = (0.06 / 1.55) x 100 = 3.87%

(2.5 marks)

(Total: 10 marks)

Report to Chief Executive Officer of Atiku Ltd on Financial Performance Relative to Obi Ltd

Introduction:

This report analyzes Atiku Ltd’s financial performance relative to Obi Ltd using four key financial ratios for the year ended 30 June 2022: operating profit margin, return on capital employed (ROCE), capital gearing, and dividend yield.

Operating Profit Margin:

Operating profit margin measures a company’s efficiency in managing its operations and generating profit from its revenue. Atiku Ltd’s operating profit margin is 13.43%, slightly lower than Obi Ltd’s 13.89%. This suggests that Obi Ltd is marginally more efficient in controlling its operating costs relative to its revenue generation.

Return on Capital Employed (ROCE):

ROCE evaluates the efficiency of a company in generating profits from its total capital employed. Atiku Ltd’s ROCE is 11.65%, compared to Obi Ltd’s 12.24%. Although the difference is marginal, Obi Ltd is slightly better at utilizing its capital to generate profit.

Capital Gearing:

Gearing shows the proportion of a company’s capital that is financed through debt. Atiku Ltd’s gearing ratio is 43.96%, compared to Obi Ltd’s 40.81%. Both companies have relatively similar gearing levels, indicating that they rely on a balanced mix of debt and equity for their capital structure. Lower gearing indicates lower financial risk, and Obi Ltd has a slight advantage in this area.

Dividend Yield:

Dividend yield shows the return on investment for shareholders based on the dividend received relative to the share price. Atiku Ltd’s dividend yield is 5.95%, higher than Obi Ltd’s 3.87%. This indicates that Atiku Ltd is offering a more attractive return to its shareholders in the form of dividends compared to Obi Ltd.

Conclusion:

Overall, the financial performance and position of both companies are quite similar. Obi Ltd has a slight edge in terms of operating efficiency and capital utilization, while Atiku Ltd offers a higher return to shareholders through dividends. Both companies exhibit relatively low gearing levels, indicating a balanced approach to financing through debt and equity.

(Total: 10 marks)