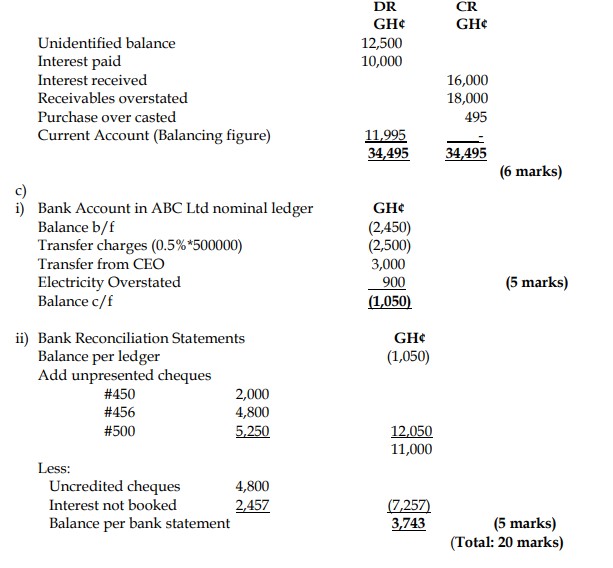

Question

Answer

a)

- Error of Omission: Failing to record a transaction. Once a transaction is omitted, it will not affect the balancing of the trial balance.

- Compensating Errors: Errors that are equal and opposite to one another, which in effect will not affect the balancing of the trial balance.

- Error of Commission: Entry recorded in the wrong accounts. For example, electricity expenses recorded as telephone expenses. This will not affect the trial balance.

- Error of Principle: Entry in the wrong class of accounts. For example, revenue expenditure treated as capital expenditure.

(2 errors well explained for 4 marks)