Question

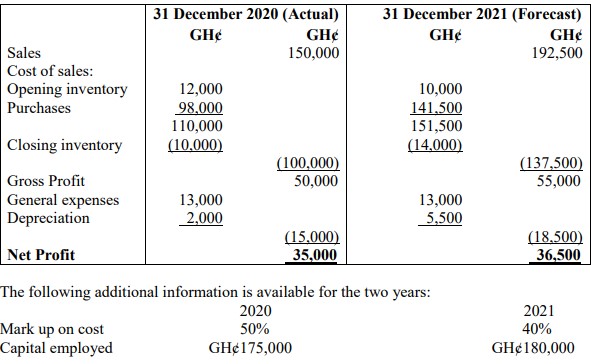

a) The accountant of Kwadaso Traders has prepared the Trading and Profit and Loss Account for the year ended 31 December 2020 and the forecast for the year ended 31 December 2021. These are reproduced below:

Required:

i) Calculate the following ratios for the year ended 31 December 2020 and for the year ended 31 December 2021.

- Gross Profit Margin (1 mark)

- Net Profit Margin (1 mark)

- Inventory Turnover (1 mark)

- Return on Capital Employed (ROCE) (1 mark)

ii) The manager of Kwadaso Traders has set the objective of improving the profitability of the business for the year ending 31 December 2021. Discuss the changes between the two years based on the ratios calculated and the additional information provided, and explain whether or not Kwadaso Traders will achieve its objective.

(8 marks)

iii) Explain the importance of the Return on Capital Employed (ROCE) percentage to a business.

(3 marks)

b) Financial statements prepared by clubs, societies, and associations are different from those prepared by sole traders, partnerships, and limited liability companies. The financial statements prepared by these not-for-profit organizations are the Trading Account, the Income and Expenditure Account, the Receipts and Payment Account, and the Statement of Financial Position.

Required:

Explain TWO (2) differences between an Income and Expenditure Account and a Receipts and Payments Account.

(5 marks)

Answer

a)

ii) Discussion of Changes and Profitability

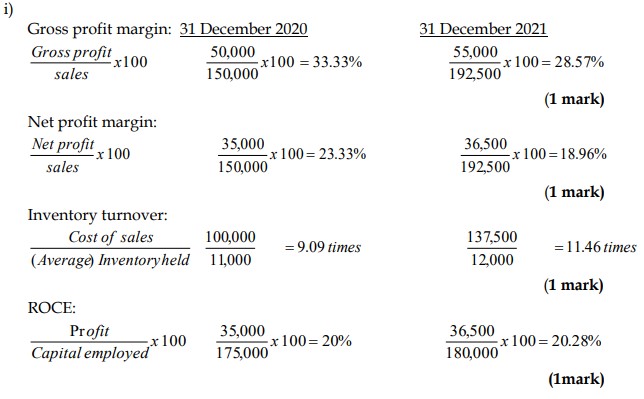

- Gross Profit Margin: The gross profit margin has decreased from 33.33% in 2020 to 28.57% in 2021, indicating that the company is either facing higher costs of goods sold or is reducing its selling prices. This could be part of a strategy to boost sales volume, but it has negatively impacted the gross profit margin.

- Net Profit Margin: The net profit margin also decreased from 23.33% in 2020 to 18.96% in 2021, reflecting the impact of increased expenses, particularly depreciation. Although the business is generating more profit in absolute terms, its profitability relative to sales has declined.

- Inventory Turnover: Inventory turnover has improved from 9.09 times in 2020 to 11.46 times in 2021, which suggests that the company is managing its inventory more efficiently, possibly due to better sales or tighter inventory controls.

- ROCE: The ROCE has slightly improved from 20.00% in 2020 to 20.28% in 2021, showing that the company is generating a slightly higher return on its capital employed, despite the reduction in profit margins. This indicates that the company is still managing to achieve its profitability objectives, albeit with reduced margins.

Conclusion:

While Kwadaso Traders has seen a decrease in profit margins, it has managed to maintain and slightly improve its ROCE, indicating that the company may still achieve its objective of improving profitability through increased efficiency and better capital utilization. However, the decline in profit margins suggests that the company should carefully monitor its cost structure.

(8 marks)

iii) Importance of ROCE

- Key Profitability Measure: ROCE is a crucial indicator of how effectively a company is using its capital to generate profits. It shows the return that the company is earning on its capital employed, which is critical for assessing the overall efficiency and profitability of the business.

- Comparison with Other Investments: ROCE allows businesses to compare the profitability of their operations with alternative investments. A higher ROCE indicates a better return on investment, making it a valuable tool for decision-making.

- Benchmarking Performance: ROCE can be used to compare the performance of a company against its peers or industry benchmarks. It helps in identifying areas where the company is performing well or needs improvement.

(3 marks)

b)

Differences between Income and Expenditure Account and Receipts and Payments Account

- Accruals vs. Cash Basis:

- The Income and Expenditure Account is prepared on an accrual basis, meaning it records income and expenses when they are earned or incurred, regardless of when cash is received or paid. It includes adjustments for prepayments, accruals, and depreciation.

- The Receipts and Payments Account, on the other hand, is prepared on a cash basis, recording only the actual cash receipts and payments during the period. It does not include any adjustments for accruals or prepayments.

- Focus on Profitability vs. Cash Flow:

- The Income and Expenditure Account aims to show the surplus or deficit for the period, reflecting the organization’s financial performance. It is similar to a profit and loss account for a for-profit business.

- The Receipts and Payments Account focuses on the cash flow of the organization, showing the opening and closing cash balances. It does not provide a measure of profitability but rather tracks the movement of cash during the period.