Question

Ugheli Limited is operating a Joint Venture with NNPC under the Year 2000 Memorandum of Understanding, while Eket Limited operates under the Sole Risk Operation agreement.

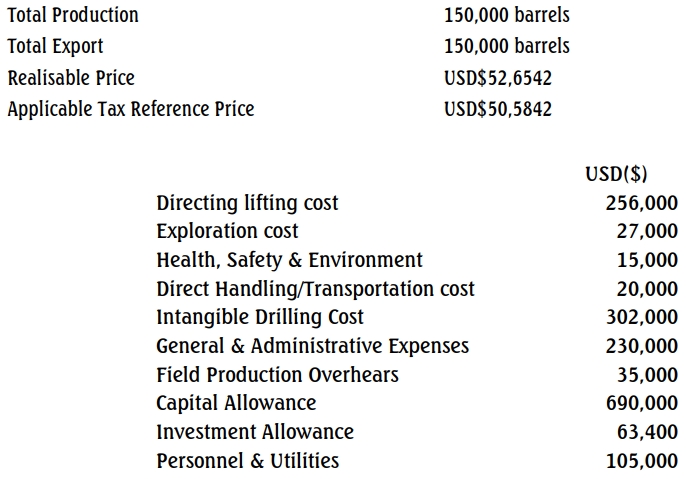

The following information reflects the two companies’ operations for the month of July 2014:

Required:

(a)

i. Using the above information, compare the effects of Incentives on Joint Venture Operation as against the Sole Risk Operation using the two companies’ operations. (7 Marks)

ii. What is the purpose of Tax Inversion Penalty (TIP)? (4 Marks)

iii. Determine the Tax Inversion Penalty and the Revised Government Take from the operations of the two companies. (Tax Inversion Rate is 35%) (3 Marks)

(b) Explain the term “Mineral Rights Acquisition Costs.” (3 Marks)

(c) Explain briefly the differences between Joint Venture and Sole Risk Agreements under the Year 2000 Memorandum of Understanding. (3 Marks)

Answer

(a)

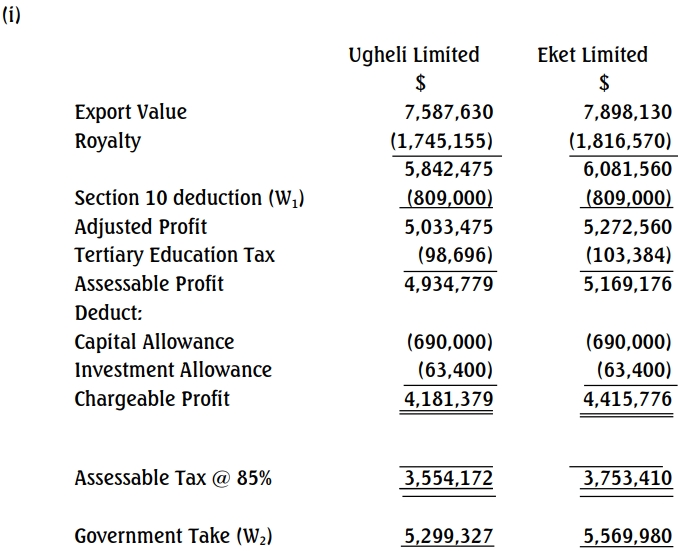

(i) Incentives for Ugheli Limited:

From the results of the operations of the two companies, the following are the incentives for Ugheli Limited:

- The Royalty payable is less than that of Eket Limited.

- The Assessable Profit of Eket Limited is higher than that of Ugheli Limited.

- The Applicable Tax Reference Price is less than the Realisable Price for Eket Limited.

- The Tertiary Education Tax of Eket Limited is higher.

- The Assessable Tax of Eket Limited is higher, as is the Government Take.

(ii) Purpose of Tax Inversion Penalty (TIP):

One of the objectives of the Year 2000 MOU is to encourage investments in the Petroleum Industry and maintain unit cost efficiency. For this purpose, the Tax Inversion Penalty (TIP) was introduced to the extent that production operating expenses (T1) are less than $1.70/bbl for any calendar year.

Formula for TIP:

TIP=(TR−TIR) ×(TI−LTIT) ×V

Where:

- TIP = Tax Inversion Penalty

- TIR = Tax Inversion Rate

- TR = Applicable Tax Rate

- TI = Allowance Deduction per Barrel

- LTIT = Lower Tax Inversion Threshold

- V = Company’s crude oil and condensate production

(iii) Tax Inversion Penalty and Revised Government Take:

Using the following data:

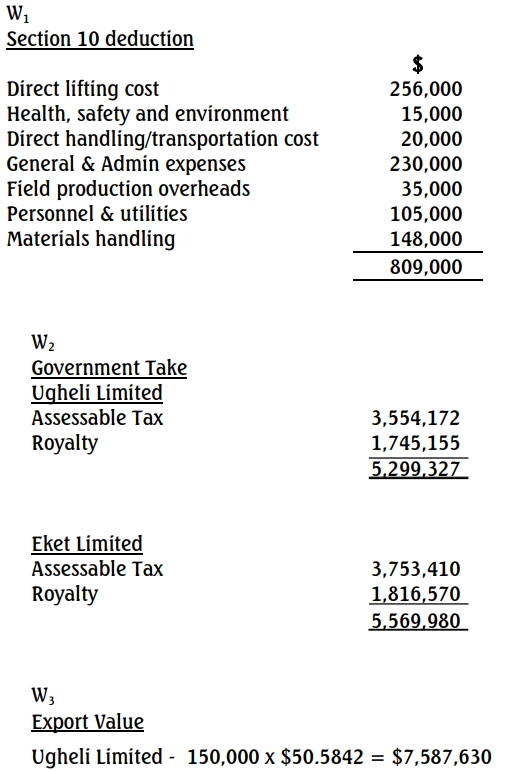

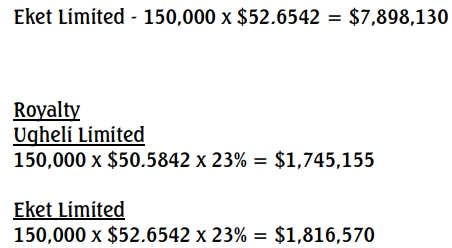

| Ugheli Limited | Eket Limited |

|---|---|

| Export Value | 7,587,630 |

| Royalty | (1,745,155) |

| Adjusted Profit | 5,033,475 |

| Tertiary Education Tax | (98,696) |

| Assessable Profit | 4,934,779 |

| Capital Allowance | (690,000) |

| Investment Allowance | (63,400) |

| Chargeable Profit | 4,181,379 |

| Assessable Tax @ 85% | 3,554,172 |

| Government Take | 5,299,327 |

- Tax Inversion Rate (TIR) = 35%

- Lower Tax Inversion Threshold (LTIT) = $1.70/bbl

Calculation for Tax Inversion Penalty (TIP):

TIP= (0.85−0.35) × (5.40−3.00) ×150,000 = 0.50×2.40 × 150,000 = 180,000

TIP = (0.85 – 0.35)

Tax Inversion Penalty = $180,000

Revised Government Take (RGT) for Ugheli Limited:

RGT= Royalty + PPT + TIP=1,745,155 + 3,554,172 + 180,000= 5,479,327

Even with the Tax Inversion Penalty, the Revised Government Take for Eket Limited remains higher.

(iv) Mineral Rights Acquisition Costs:

Mineral Rights Acquisition Costs are incurred in acquiring concession rights to a lease area. These include:

- Signature Bonus: The initial payment made by the lessee to the lessor.

- Legal Fees: Costs associated with the legal acquisition of the property.

- Local Statutory Land Acquisition Fees/Levies: Costs related to land and mineral rights acquisition.

- Reserves Value Fees: Fees paid for the reserves’ value.

Acquisition costs may relate to both proved and unproved properties. Costs incurred to purchase, lease, or otherwise acquire properties are capitalized when incurred. These costs include:

- Oil Prospecting License (OPL): Granted to search for oil.

- Oil Exploration License (OEL): Permits exploration for petroleum.

- Oil Mining Lease (OML): Allows winning, working, and carrying away petroleum.

- Bonuses and Options to Purchase or Lease Properties: Payments made for these rights.

- Minerals: When land, including mineral rights, is purchased.

- Recording Fees: Costs related to legal recording and other acquisition processes.

Pre-licensing Costs refer to costs incurred before obtaining the legal right to explore for oil and gas in a location. These include:

- Speculative Seismic Data Acquisition

- Geological and Geophysical Analysis of Data

(c) Joint Venture

Joint venture is a contractual agreement whereby two or more parties undertake an economic activity which is subject to contractually agreed basis of sharing of control.

Under the Joint venture contract (JVC), each company is required to enter into joint contract agreement with the NNPC in respect of the company’s operations in a particular oil field. The basis of the right and obligation are spelt out in the agreement.

A party in the agreement is given the concession to conduct the operations of drilling of a well/and/or the production of Oil.

Each party is allowed to lift from the crude oil produced, its equity share. NNPC equity contribution to the cost of operation is regarded as cash call.

Sole Risk Operation

Under the Sole Risk Operation, the operator (mostly indigenous operators) is allowed to operate on its own. The operator bears the cost of operations and when it discovers and produces oil in commercial quantity, it pays tax and royalty to the government. In most cases, the indigenous operators always go into technical agreements with overseas technical partners. As the name implies the operator bears the entire 100% risk.