Question

Answer

a) Capital Allowance Computation:

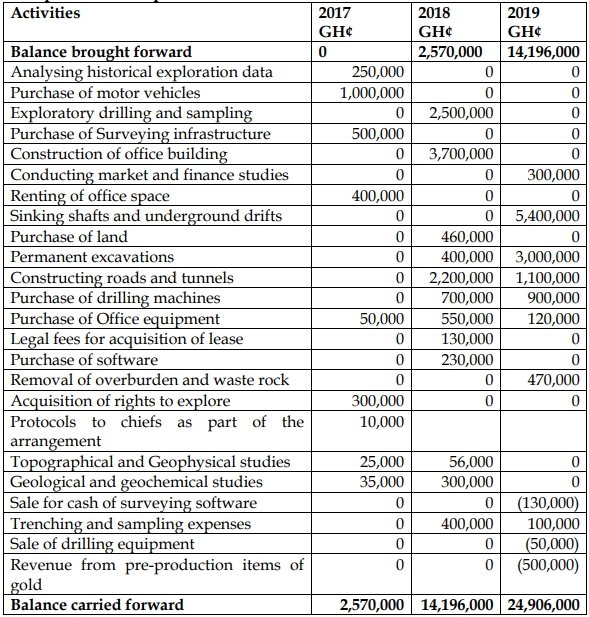

Reconnaissance and Prospecting Expenditure as at 1 January 2020: GH¢24,906,000

Additional capital expenditure in 2020:

- Iron Gate: GH¢421,600

Total capital expenditure: GH¢25,327,600

Capital Allowance (20% of GH¢25,327,600) = GH¢5,065,520

b) Chargeable Income and Tax Payable for 2020:

| Description | Amount (GH¢) | Total (GH¢) |

|---|---|---|

| Sales of gold and diamonds | 378,532,900 | |

| Compensation received | 3,500,000 | |

| Total Revenue | 382,032,900 | |

| Less: Allowable Expenses | ||

| Mining and processing cost | (120,345,000) | |

| Ground rent | (321,500) | |

| Royalties | (11,355,987) | |

| Stope preparation and development | (1,021,700) | |

| Business operating permits (excluding 2021) | (5,163,200) | |

| General and administrative expenses (excl. gate) | (190,045,500) | |

| Selling and distribution costs | (172,554,700) | |

| Finance costs | (211,500,000) | |

| Capital allowance | (5,065,520) | |

| Total Allowable Expenses | (717,373,107) | |

| Loss Carried Forward | (335,340,207) | |

| Tax Payable: No tax payable due to the loss carried forward. |

c) Tax Treatment of Royalty Payments and New Mineral Rights:

- Royalty Payments:

Royalties are levied on production and are an allowable deduction for tax purposes. In this case, the royalty of GH¢11,355,987 paid by Kanawu Mine Resources Ltd is deductible when calculating the company’s chargeable income. - New Mineral Rights Acquisition:

The acquisition of a new mineral right is considered a capital asset and should be capitalized. Capital allowances will be granted on this asset. Since the acquisition is related to a new mining operation, it will be treated as a separate mineral operation.