Question

Answer

i) Reasons for Converting to a Limited Liability Company

- Branch profit tax: External companies are subject to a branch profit tax of 8%. Converting to a limited liability company eliminates this.

- Interest on loans: Loans from the parent company are treated as loans to oneself in the case of an external company and are non-deductible. Conversion resolves this.

- Legal autonomy: An external company cannot sue in its name; it is the parent company that sues. A limited liability company can sue and be sued in its own name.

(Any 3 points, 1 mark each = 3 marks)

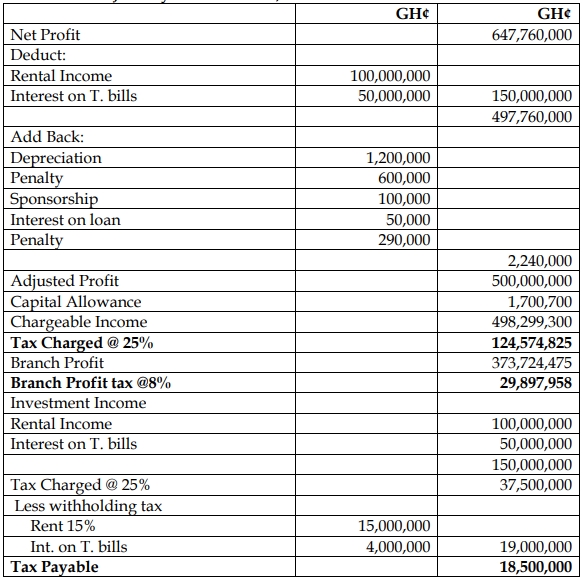

ii) Tax Payable and Branch Profit Tax Computation

Thunder Ltd

Computation of Branch Profit Tax

Year of assessment 2021

Basis Period 1st January – December 31, 2021

iii) Tax Implications of Conversion

- The conversion of an external company to a limited liability company would require issuing shares as the stated capital or converting the head office investment into stated capital.

- Additionally, a stamp duty of 0.5% will be paid on the stated capital.