Question

Finstruct Ltd has been awarded an airport terminal project. The project started on 1 January 2022 for a contract sum of GH¢60,000,000. The construction of the airport is to be completed on 31 December 2023.

Finstruct Ltd has a financial year ending on 31 December each year. On 31 December 2022, the accounts appropriate to the airport contract contained the following:

| Cost Item | GH¢ |

|---|---|

| Cost of construction materials | 25,500,000 |

| Direct wages of construction staff | 22,100,000 |

| Hire of special equipment | 300,000 |

| Cost of soil test | 100,000 |

| Purchase of fuel and lubricants | 750,000 |

| Consultancy services | 135,000 |

Additional information:

i) Materials costing GH¢340,000 sent to the site were returned to the company’s warehouse.

ii) Materials sent to the site worth GH¢675,000 were still unused at the construction site as of 31 December 2022.

iii) Finstruct Ltd pays some of its workers the first week of the ensuing month after the end of the current month. GH¢57,000 is still owed for wages as of the close of the year 2022, and this was not included in the accounts.

iv) A bill amounting to GH¢45,000 was submitted late by Finstruct Ltd, and as of 31 December 2022, the bill had not yet been paid. This was not included in the accounts.

v) It is estimated that the cost to complete the project as of 31 December 2022 should be GH¢8,265,180.

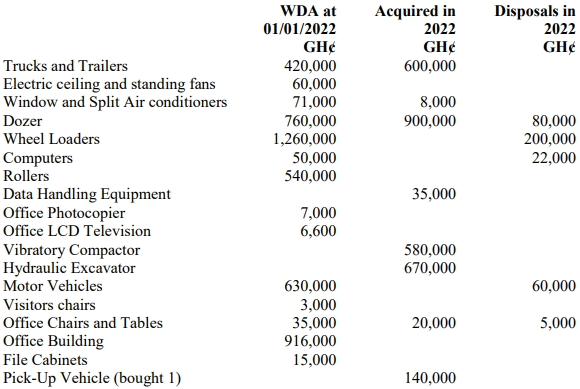

vi) The following details are available on assets of Finstruct Ltd:

Required:

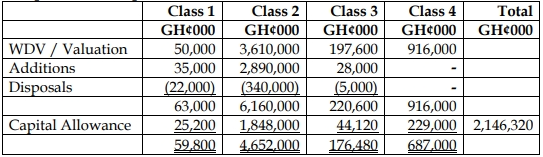

a) Compute the capital allowance for Finstruct Ltd for the year 2022. (6 marks)

b) Explain the tax rules on long-term contracts and compute the percentage of contract completion of the project. (4 marks)

c) Compute the chargeable income of Finstruct Ltd for the year ended 31 December 2022. (10 marks)

Answer

a)

Computation of Capital Allowance

Assumptions:

1. There was no depreciation

2. Pick up was not restricted because of the nature of the sector

b) Explanation of Tax Rules on Long-Term Contracts and Calculation of Percentage Completion

Amounts to be included or deducted in calculating the person’s income related to a long-term contract are considered based on the percentage of the contract completed during each basis period. The percentage of completion is determined by comparing the total expenses allocated to the contract and incurred before the end of a basis period with the estimated total contract expenses as determined at the time of commencement of the contract.

Percentage of Completion =![]() 85.84%

85.84%

(4 marks)

c) Computation of Chargeable Income for Finstruct Ltd for the year ended 31 December 2022

| Description | GH¢ |

|---|---|

| Materials to site | 25,500,000 |

| Less: Materials returned | (340,000) |

| Less: Closing stock (Unused materials) | (675,000) |

| Net Material Cost | 24,485,000 |

| Wages Paid | 22,100,000 |

| Add: Wages Owed | 57,000 |

| Net Wages Cost | 22,157,000 |

| Hire of Special Equipment | 300,000 |

| Cost of Soil Test | 100,000 |

| Fuel and Lubricant | 750,000 |

| Consultancy Services | 180,000 |

| Capital Allowance | 2,146,320 |

| Total Cost to Date | 50,118,320 |

| Estimated Cost to Complete | 8,265,180 |

| Total Cost of Completion | 58,383,500 |

Stage of Completion = 85.84%

Revenue: 85.84% x GH¢60,000,000 = GH¢51,504,000

Cost of Sale: 85.84% x GH¢58,364,000 = GH¢50,099,658

Chargeable Income: GH¢1,404,342