Question

Answer

i) The tax implication of a resident entity holding 25% of another resident entity is that,

any dividend declared is exempt from tax. This does not, however, apply if the paying

company is into mining and mineral operations or petroleum operations.

(1.5 marks)

ii) Income accrued and derived by non-resident is payable in Ghana and the global

income of resident person is payable in Ghana. It is therefore wrong for PAYE

payment of Citizens of United Kingdom be payable in United Kingdom. It has to be

paid in Ghana.

(1.5 marks)

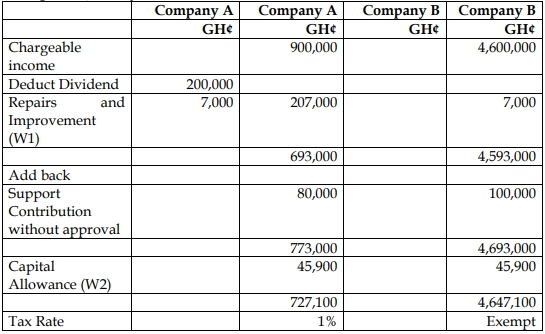

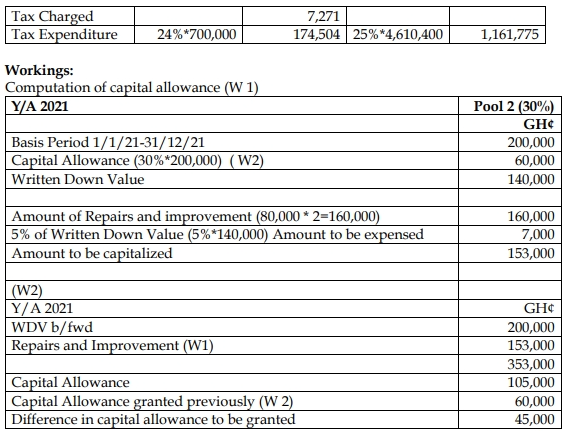

iii) Computation of tax payable and Tax Expenditure

Year of assessment 2021

Basis period January 1, 2021 to December 31, 2021