Question

Answer

a. Reasons Why a Business May Cease Trading:

-

- Government Policy Changes: Regulatory changes, such as import restrictions or trade barriers, can negatively impact business viability.

- Financial Challenges: Consistent losses or cash flow issues can lead to an inability to meet operational costs, prompting closure.

- Market Conditions: Increased competition, declining demand, or economic downturns may force a business to cease operations.

b. Raposa Nigeria Limited

Computation of net terminal adjusted profit

The net terminal adjusted profit was N500,000

NOTE:

(i) Bad debts recovered in October 2021 must have been captured in the relevant accounting year.

(ii) Amount spent in recovering the debt must also have been captured in the same accounting year.

(iii) The expenditure of N350,000 was actually passed through the books before the year of cessation.

Given the fact that the transactions occurred before the date of cessation, informed the decision to ignore same in the computation of the net terminal adjusted profit.

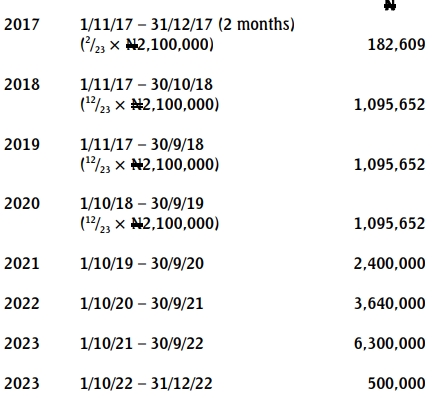

c. Raposa Nigeria Limited

Computation of assessable Profit

For the relevant assessment years