Question

Answer

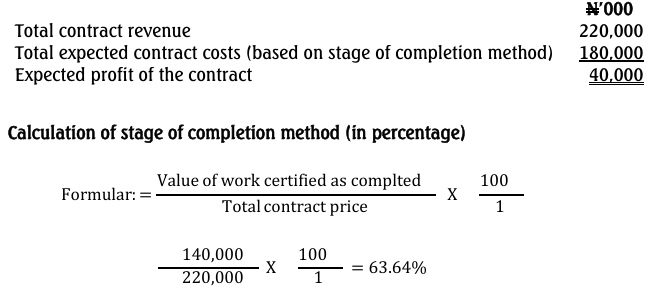

a. Calculation of expected profit of the contract at December 31, 2019

Determination of the amount to be recognised in Housing-for-all Corporation‟s income statement

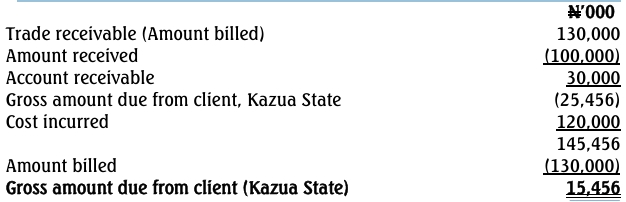

b. Calculation of amount to be recognised in the statement of financial position for gross amount due to or from client, Kazua State and accounts receivable

Housing-for-all Corporation

Income statement extracts for the year ended December 31, 2019

Housing-for-all Corporation

Statement of financial position extracts as at December 31, 2019

c. Composition of Major Contract Costs as Contained in IPSAS 11

- Site labour costs, including site supervision.

- Cost of materials used in construction.

- Depreciation of plant and equipment used on the contract.

- Cost of moving plant, equipment, and materials to and from the contract site.

- Cost of hiring plant and equipment.

- Costs of design and technical assistance directly related to the contract.

- Estimated costs of rectification and guarantee work, including expected warranty costs.

- Claims from third parties.

- Costs attributable to contract activity in general and allocable to the contract on a systematic basis.

- Other specifically chargeable costs under the terms of the contract.