Question

Answer

a. Provisions of the VAT Law with Regard to Rendition of Returns by Vatable Persons (2 Marks)

- Monthly Filing Requirement: Under the Value Added Tax (VAT) Act, all vatable persons are required to file VAT returns with the Federal Inland Revenue Service (FIRS) on a monthly basis, no later than the 21st day of the month following the month in which the transaction occurred.

- Exempt Goods: Even if a taxpayer deals in VAT exempt goods, they are still required to file NIL returns to comply with regulatory requirements.

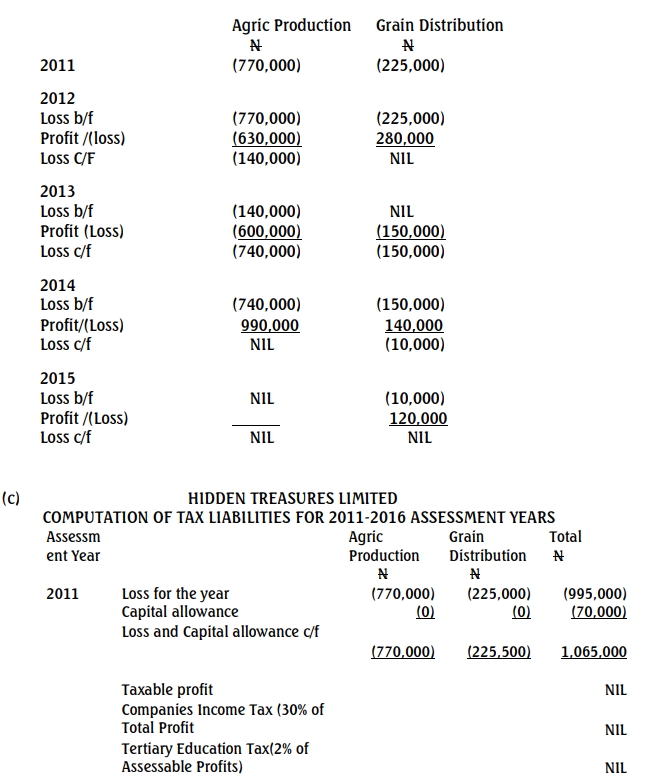

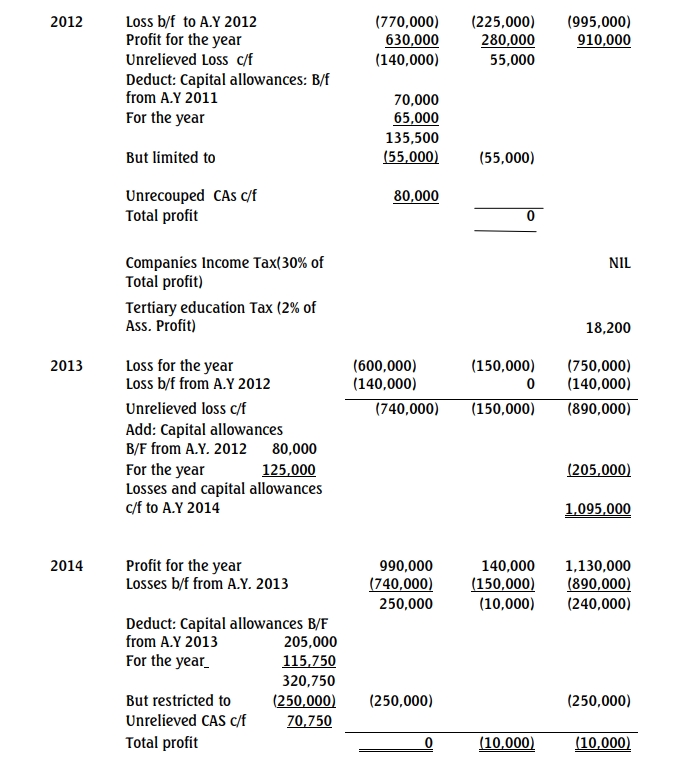

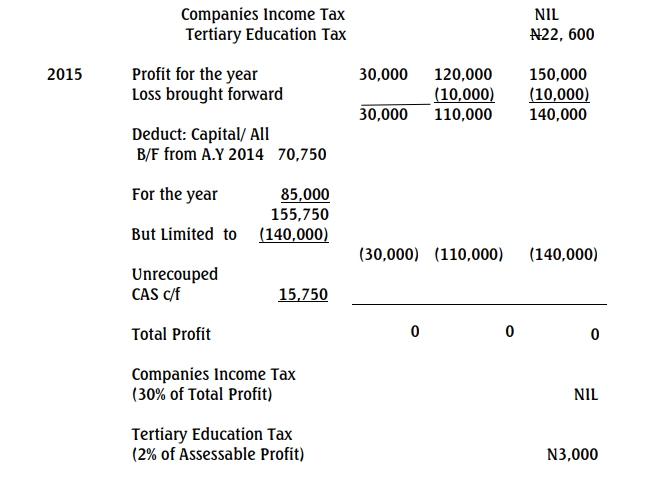

b. Analysis of Losses Carried Forward Under Each Income Head (8 Marks)