Question

You have been invited to make a presentation to the Board of Directors of BICCI Nigeria Limited. Your performance at the presentation will determine your appointment as the Tax Consultant to the company.

BICCI Nigeria Limited, a trading company, was incorporated on 2 March 2009. It commenced business on 2 October of the same year, making accounts up to 30 September annually. The shareholders invested N18 million in non-current assets before the company commenced business in 2009.

Other information provided:

- Authorized, Issued, and Fully Paid-Up Capital – N10 million.

- Value Added Tax (VAT) and Withholding Tax (WHT) returns filed for 2010–2013 were carried out 2 months after each transaction month.

- Companies Income Tax (CIT) and Tertiary Education Tax (TET) returns were filed on 30 June for the 2011 to 2014 Assessment Years.

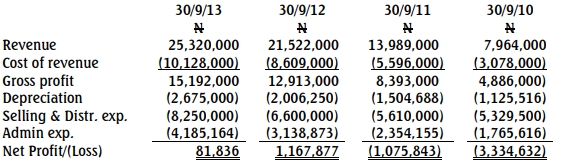

Extracts from the accounts (2010–2013):

On 15 July 2014, FIRS inspectors visited BICCI, informing management of an upcoming tax audit on 25 August 2014. They requested the following documents:

- Audited Accounts (2010–2013)

- Bank Statements (2010–2013)

- Trial Balance for each year

- Evidence of Tax Returns filed (CIT, VAT, WHT, TET)

- General Ledger printouts

- Proof of tax payments

- Tax registration evidence

- Tax Clearance Certificates

- WHT Credit Notes, if any

FIRS Interim Tax Audit Report (summarized):

| Item | 2013 | 2012 | 2011 | 2010 |

|---|---|---|---|---|

| Revenue (N’000) | 25,320 | 21,522 | 13,989 | 7,694 |

| VAT on Revenue | 8,862 | 7,533 | 4,896 | 3,462 |

| Undisclosed Revenue | 16,458 | 13,989 | 9,093 | 4,232 |

| Directors’ Current Account | 19,578 | 21,228 | 19,250 | 18,000 |

| Payments under WHT: | ||||

| – Directors’ Fees | 1,625 | 2,125 | 1,145 | 960 |

| – Rent | 3,500 | 3,500 | 2,625 | 2,625 |

| – Professional Fees | 1,200 | 1,200 | 950 | 950 |

| – Commission | 2,825 | 1,875 | 970 | 376 |

Additional Adjustments:

- Cost of Sales written back: 60%

- Selling & Distribution expenses written back: 60%

- Admin expenses written back: 60%

Requirements:

a. List the documents required by FIRS for the Interim Tax Audit. (3 Marks)

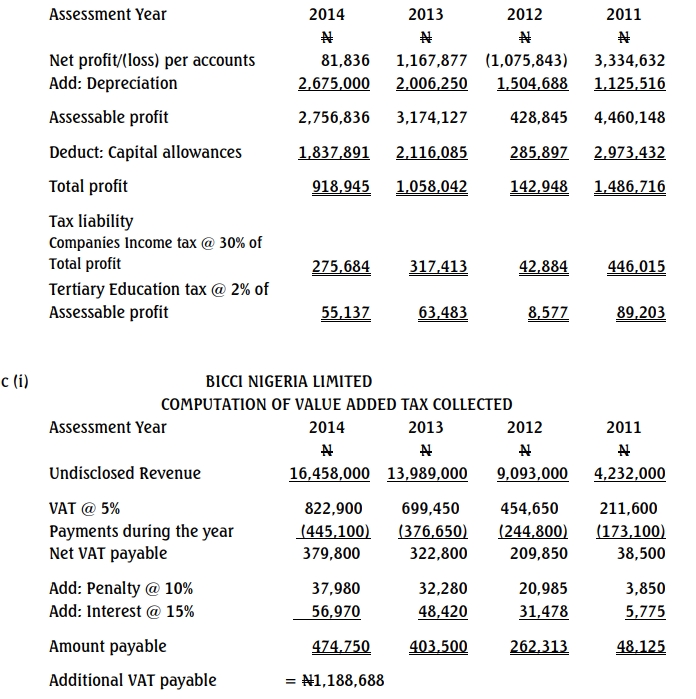

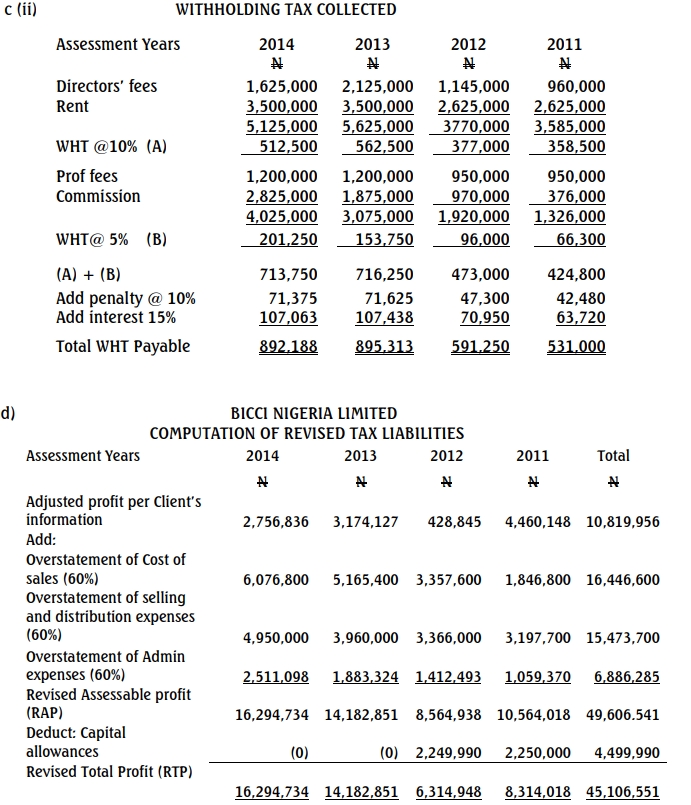

b. Calculate BICCI Nigeria Limited’s potential tax liabilities per the Interim Tax Audit. (12 Marks)

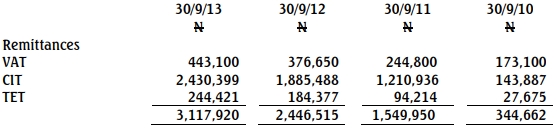

c. Prepare a schedule for VAT and WHT receipts collected by BICCI. (7 Marks)

d. Advise management on possible tax consequences if they do not respond to the audit. (8 Marks)

Answer

a. Documents Required by FIRS:

- Audited Accounts (2010–2013)

- Bank Statements (2010–2013)

- Trial Balances (Annual)

- Evidence of Filed Returns: CIT, VAT, WHT, TET

- General Ledger Printouts

- Proof of Tax Payments

- Tax Registration Certificate

- Tax Clearance Certificates (Annual)

- WHT Credit Notes (If any)

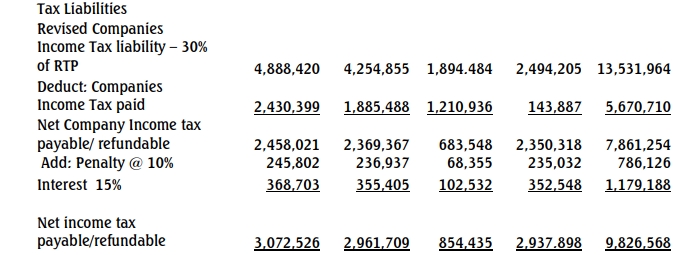

b. Computation of Possible Tax Liabilities:

Advice on Non-Compliance with FIRS Audit

If BICCI Nigeria Limited does not respond to the FIRS audit, the following consequences may apply:

- Penalty for Non-Compliance: The FIRS may impose severe penalties for failing to comply, which can lead to escalated financial obligations for BICCI.

- Interest Accumulation: Unpaid tax liabilities accrue interest, increasing the company’s overall financial liability.

- Legal Action: Persistent non-compliance can lead to legal proceedings, where the FIRS may pursue asset seizures or additional sanctions.

- Reputational Damage: Tax non-compliance may damage BICCI’s reputation, impacting future business prospects and investor confidence.

It is recommended that BICCI Nigeria Limited provides all required documentation promptly, negotiates any disputed assessments, and settles outstanding liabilities to avoid these penalties.