Question

Hurricane Limited

You are the audit manager in charge of the audit of Hurricane Limited. The company’s year-end is 31 December, and Hurricane Limited has been a client for seven years. The company purchases and resells fittings for ships, including anchors, compasses, rudders, sails, etc. Clients vary in size from small businesses making yachts to large companies maintaining large luxury cruise ships. No manufacturing takes place in Hurricane Limited.

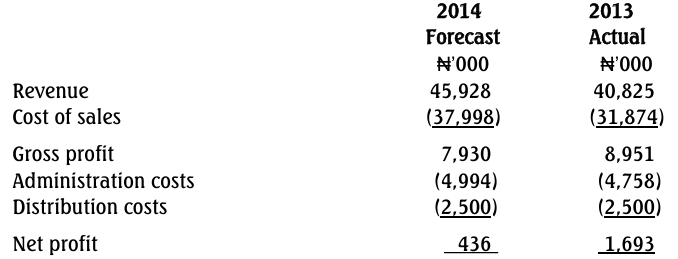

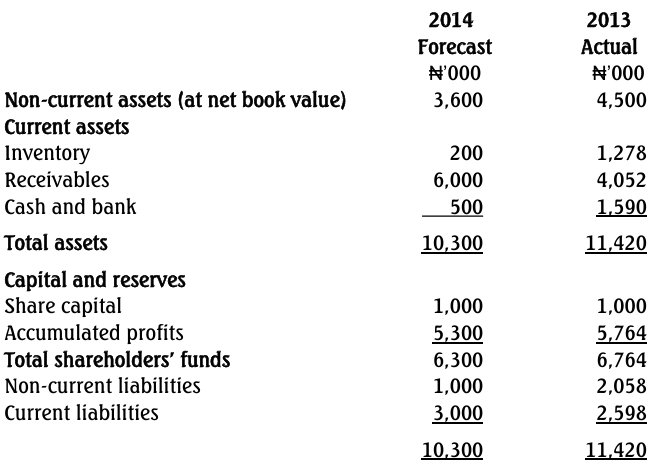

Information on the company’s financial performance is available as follows:

Other Information:

i. The industry in which Hurricane Limited operates has seen moderate growth of 7% over the last year.

ii. Non-current assets mainly relate to company premises for storing inventory. Ten delivery vehicles are owned with a net book value of ₦300,000.

iii. One of the directors purchased a yacht during the year.

iv. Inventory is stored in ten different locations across the country, with your firm again having offices close to seven of those locations.

v. A computerized inventory control system was introduced in August 2013.

vi. Inventory balances are now obtainable directly from the computer system. The client does not intend to count inventory at the year-end but relies instead on the computerized inventory control system.

Required:

a. ISA 300 Planning an Audit of Financial Statements, states that an auditor must plan the audit.

Explain why it is important to plan an audit. (5 Marks)

b. Using the information provided above, prepare the audit strategy for Hurricane Limited for the year ending 31 December 2014. (15 Marks)