Question

Answer

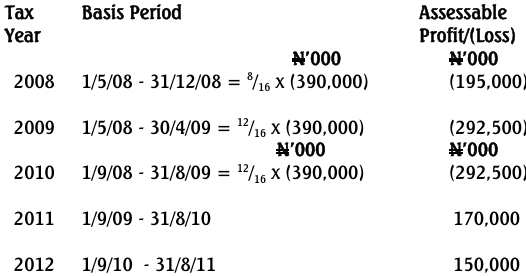

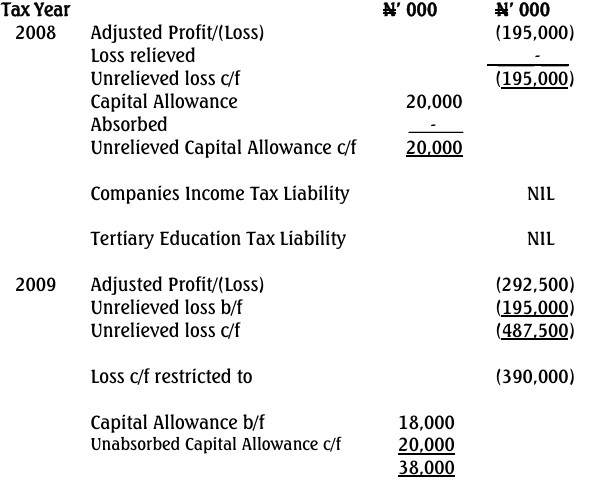

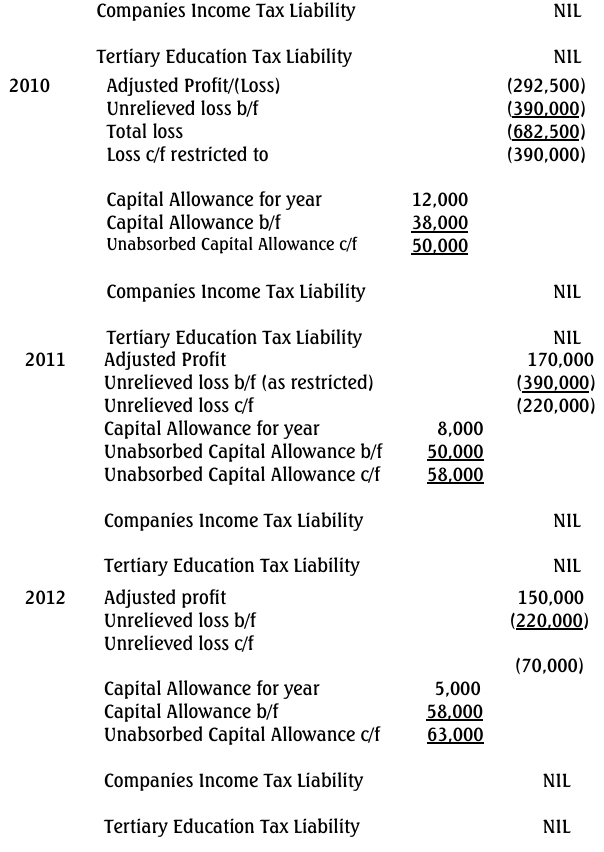

a. Determination of Basis Period and Tax Liabilities for Gab Pal Limited:

Computation of Tax Liabilities for the relevant years

b. Two Types of Loss Reliefs Acceptable to the Tax Authority:

- Current Year Loss Relief: Allows setting off the trade loss against profits from the same trade in the current tax year.

- Carried Forward Loss Relief: Enables carrying forward unutilized trade losses to future years to offset against profits from the same trade.

c. Conditions for Enjoying Loss Reliefs:

- For Current Year Loss Relief:

- The trade loss must be set off against the current year’s income from the same trade.

- The relief applies only to trade losses, not against other income sources.

- For Carried Forward Loss Relief:

- It applies to trade losses from the preceding year.

- This relief is automatically applied against income from the same trade in future years.

- The loss must not have been relieved under Current Year Loss Relief.

- It can be carried forward indefinitely except for insurance companies.

d. Conditions for Granting Capital Allowances:

- The company must have incurred qualifying capital expenditure.

- The company must remain the beneficial owner of the asset at the end of the basis period.

- The asset must be used wholly, exclusively, and necessarily for the business.

- For assets over ₦500,000, an Acceptance Certificate is required from the Federal Ministry of Industry, Trade, and Investment.