Question

Answer

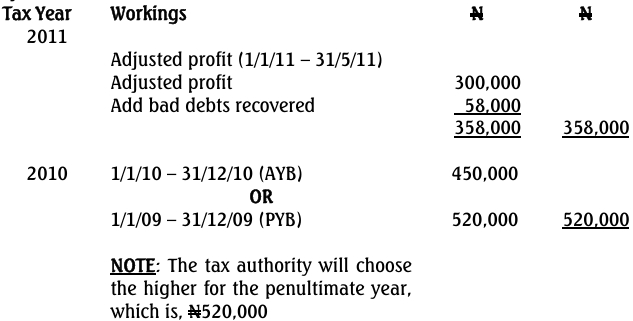

a. Computation of Assessable Profits for the Relevant Assessment Years

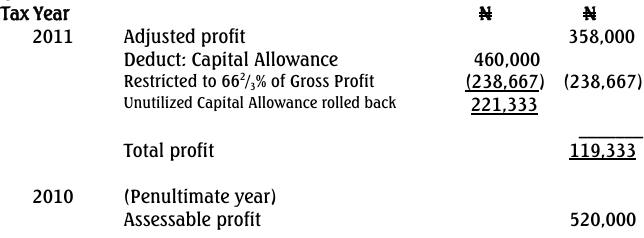

b. Capital Allowances to be Rolled back to the Relevant Years

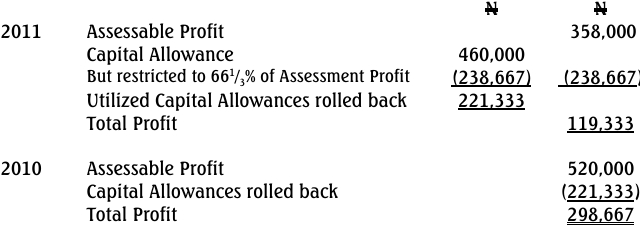

c. Total Profits of the Relevant Years of Assessment

d. Best of Judgment (BoJ) Assessment Explanation:

A Best of Judgment (BoJ) Assessment is applied when a taxpayer fails to submit accurate returns or records. The tax authorities estimate the tax liability based on available information or assumptions to ensure compliance, especially when financial statements are deemed unreliable.