Question

a. Accounting for deferred tax is based on the identification of temporary differences.

Required:

Explain the term “Temporary difference” and discuss the TWO different types. (3 Marks)

b. State and briefly explain FIVE components of tax expense or income. (5 Marks)

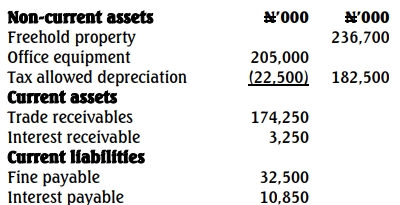

c. Buga Nigeria Limited had an accounting profit before taxation of N196,800,000 for the year ended September 30, 2022. The following balances were extracted from the company’s books as at September 30, 2022.

Other information:

- Interest income is taxed while interest expense is allowable on a cash basis. There were no opening balances on interest receivable and interest payable.

- The trade receivables above are shown net of an allowance for doubtful balances of N16,750,000. This is the first year that such an allowance has been recognized. A deduction for debts is only allowed for tax purposes when the debtor is in the process of winding-up.

- The balances in respect of office equipment are after charging accounting depreciation of N28,250,000 and tax allowable depreciation of N22,500,000 respectively.

- The freehold property was purchased on October 1, 2021, for N263,000,000 and is being depreciated for accounting purposes on a 10% per annum basis. Buga Nigeria Limited is in a position to claim N94,600,000 as accelerated depreciation on cost as a taxable expense in this year’s tax computation.

Required:

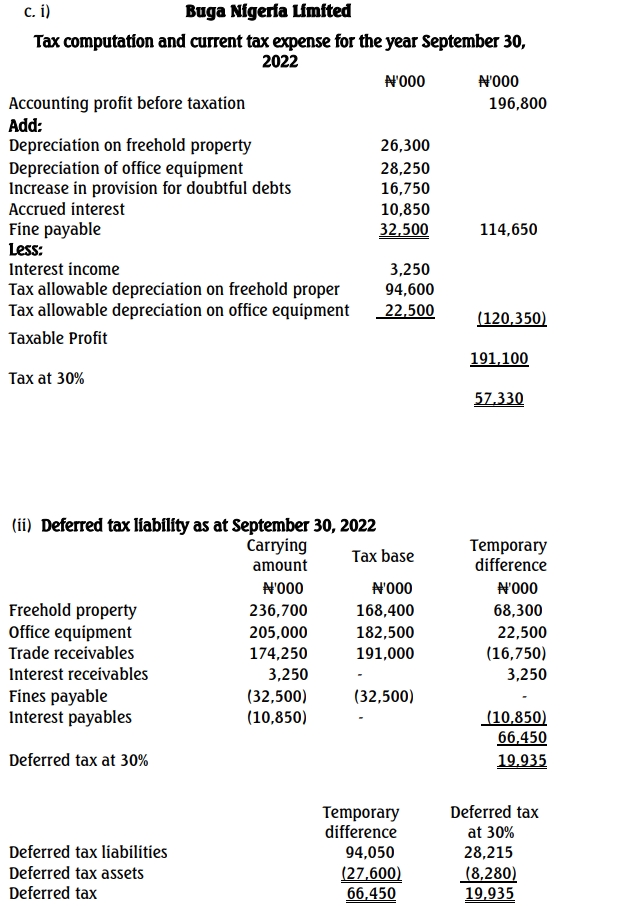

i. Prepare a tax computation and calculate the current tax expense. (4 Marks)

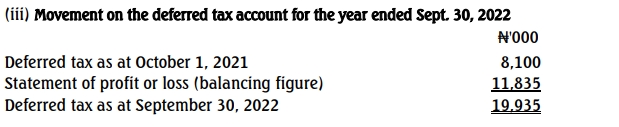

ii. Calculate the deferred tax liability as at September 30, 2022. (6 Marks)

iii. Show the movement on the deferred tax account for the year ended September 30, 2022, given that the opening balance was N8,100,000. (2 Marks)

Answer

Part a:

Explanation of “Temporary Difference”

- Temporary Differences: Temporary differences are differences between the carrying amount of an asset or liability in the statement of financial position and its tax base. These differences will result in taxable or deductible amounts in the future when the carrying amount of the asset is recovered or the liability is settled.

- Taxable Temporary Differences:

These are temporary differences that will result in taxable amounts in determining taxable profit (or tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled. For example, if a company has a higher accounting profit due to different depreciation methods compared to tax depreciation, this creates a taxable temporary difference. - Deductible Temporary Differences:

These are temporary differences that will result in amounts that are deductible in determining taxable profit (or tax loss) of future periods. An example is when expenses are recognized in the financial statements before they are allowed for tax purposes, such as provisions for warranties that are recognized in the current year but will only be deductible when paid.

Part b:

Components of Tax Expense or Income

- Current Tax Expense or Income:

This represents the amount of income tax payable (or recoverable) based on the taxable profit of the current year, calculated at the applicable tax rate. - Adjustments for Prior Periods:

This includes any adjustments recognized in the current period for current tax related to prior periods. These adjustments may arise from audits or reassessments by tax authorities. - Deferred Tax Expense or Income:

This is the amount of tax expense or income arising from the origination and reversal of temporary differences. It reflects the expected tax consequences of the differences between the carrying amounts of assets and liabilities in the financial statements and their tax bases. - Changes in Tax Rates:

Any deferred tax expense or income relating to changes in tax rates or the imposition of new taxes during the reporting period. - Unrecognized Tax Losses or Credits:

The amount of the benefit from previously unrecognized tax losses, tax credits, or temporary differences of prior periods that are now being used to reduce the deferred tax expense.

Part c:

Tax Computation and Current Tax Expense