Question

Answer

TEE COMPANY

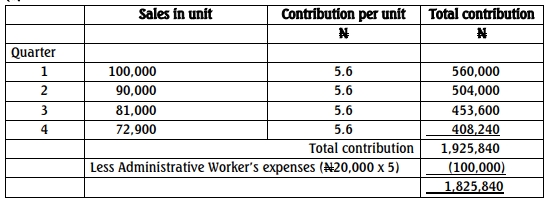

(a) Green Product

Note: Fixed cost is not relevant in decision making Brace Product

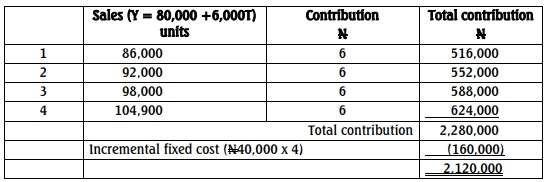

Based on the above analysis, Brace Product should be introduced in Year 7 to

produce additional contribution of N294,160 i.e. N2,120,000 – N1, 825,840.

(b) Brace Product

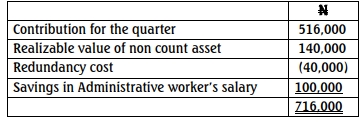

(i) Analysis of Revenue and cost if changeover is on the 1st of January

Brace Product

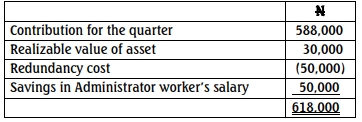

(ii) Analysis of cost and revenue if the changeover is on the 1st of July

Note

(i) Written down value of asset is a combination of historical cost and

depreciation that are both irrelevant. Therefore, assets that are no

longer required will have only realizable value to the holders.

(ii) Savings in Administrative workers‟ salary will be 100% saved, if

changeover takes place in January 1st. In contrast, if changeover

takes place on 1st July, only 50% will be saved.