Question

Answer

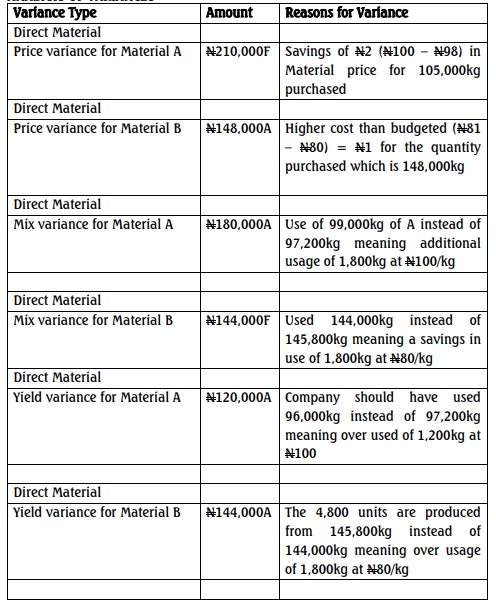

a) i) Material Price Variance

= AQP (SP – AP)

A 105,000(100 – 10,290,000/105,000) = ₦210,000 (F)

B 148,000(80 – 11,988,000/148,000) = ₦148,000 (A)

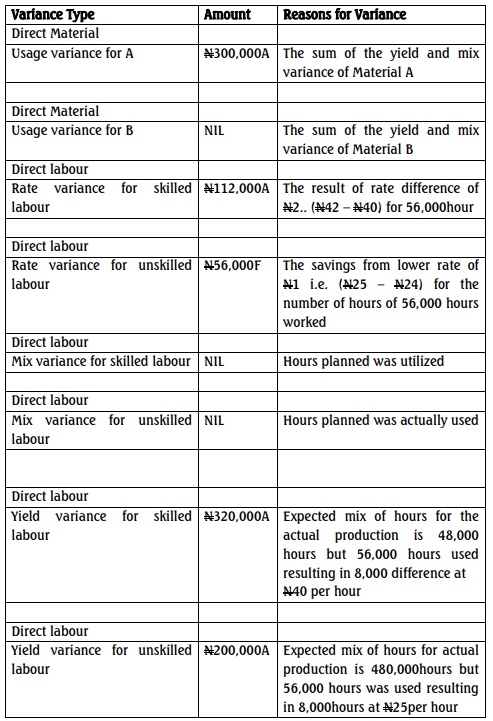

ii) Material Usage Variance:

= SP(SQ – AQ used)

A 100[(4,800 × 20kg) – 99,000] = ₦300,000 (A)

B 80[(4,800 × 30kg) – 144,000] = ₦0

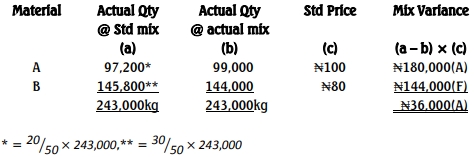

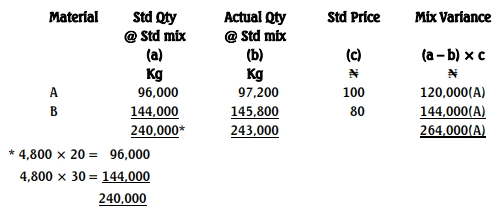

iii) Material Mix Variance

iv) Material Yield Variance

v) Labour Rate Variance = AH (SR – AR)

Skilled 56,000(₦40 – ₦2,352,000/56,000) = ₦112,000(A)

Unskilled 56,000(₦25 – ₦1,344,000/56,000) = ₦56,000(F)

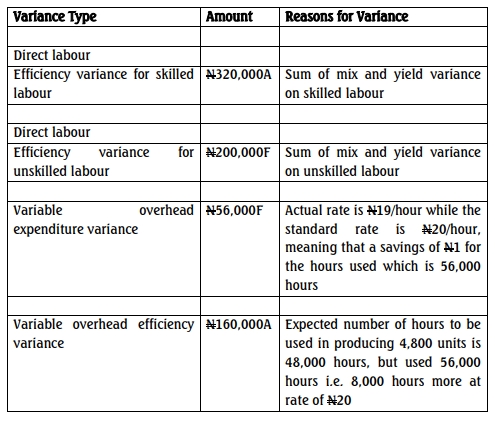

vi) Labour Efficiency Variance

= SR(SH – AH)

Skilled ₦40[(4,800 × 10hrs) – 56,000] = ₦320,000(A)

Unskilled ₦25[(4,800 × 10hrs) – 56,000] = ₦200,000(A)

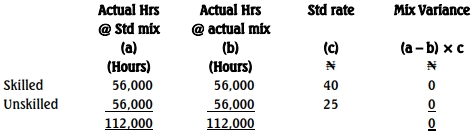

vii) Labour Mix Variance

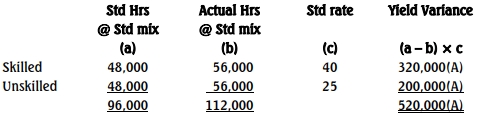

viii) Labour Yield Variance

xi) Variable Overhead Expenditure Variance

= AH (SR – AR)

= 56,000(₦20 – ₦1,064,000/56,000) = ₦56,000(F)

x) Variable Overhead Efficiency Variance

= SR (SH – AH)

= ₦20[(4,800 × 10hrs) – 56,000] = ₦160,000(A)

(b) Possible Causes of the Variances:

- Material Price Variance:

- Material A (Favorable): Likely due to efficient negotiation or purchasing a lower-grade material.

- Material B (Adverse): Likely due to unexpected increases in market prices or inaccurate budget standards.

- Material Usage Variance:

- Material A (Adverse): Possibly caused by inferior material quality or inexperienced operatives leading to excess usage.

- Material B (Favorable): Effective material utilization or careful handling.

- Labour Rate Variance:

- Skilled Labour (Adverse): Likely due to employing higher-paid skilled workers or unexpected wage rate increases.

- Unskilled Labour (Favorable): Possibly due to hiring at lower wage rates or efficient negotiation.

- Labour Efficiency Variance:

- Skilled and Unskilled Labour (Adverse): Poor quality raw materials, high rework rates, machine issues, power outages, or inadequate supervision.

- Variable Overhead Variance:

- Expenditure (Favorable): Savings from efficient overhead cost control.

- Efficiency (Adverse): Overuse of hours possibly due to low efficiency in production operations.

Note: credit will be given for alternative relevant points

b) ANALYSIS OF VARIANCES