Question

Answer

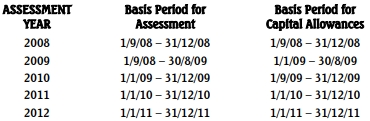

JOHNGAB LIMITED

DETERMINATION OF BASIS PERIODS

FOR THE RELEVANT ASSESSMENT YEARS AND CAPITAL ALLOWANCESS

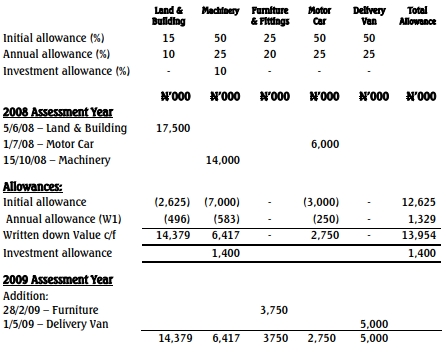

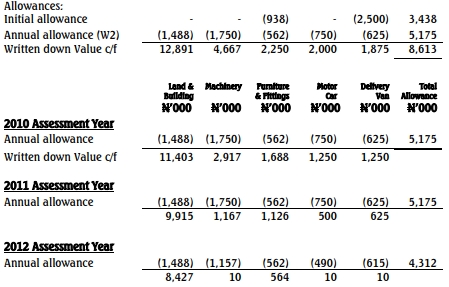

(b) COMPUTATION OF CAPITAL ALLOWANCES

DUE FOR 3 YEARS

Note: Since the Capital Allowance is less than 3/2 of Assessable Profit for each of the relevant years, all the Capital Allowances are claimable.