Question

Answer

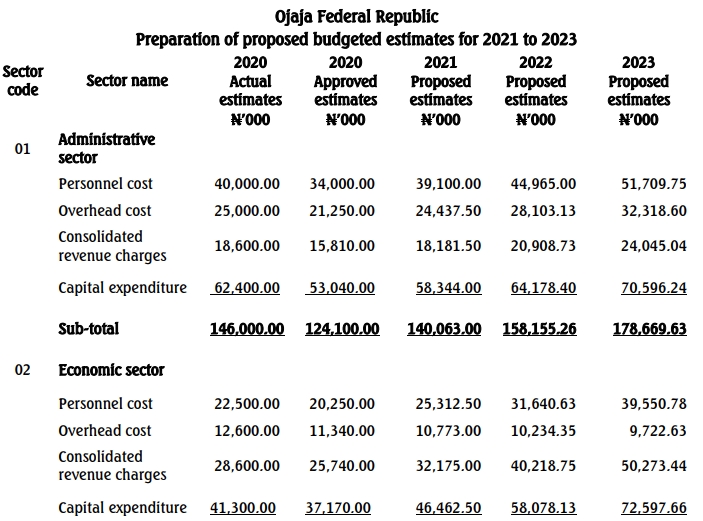

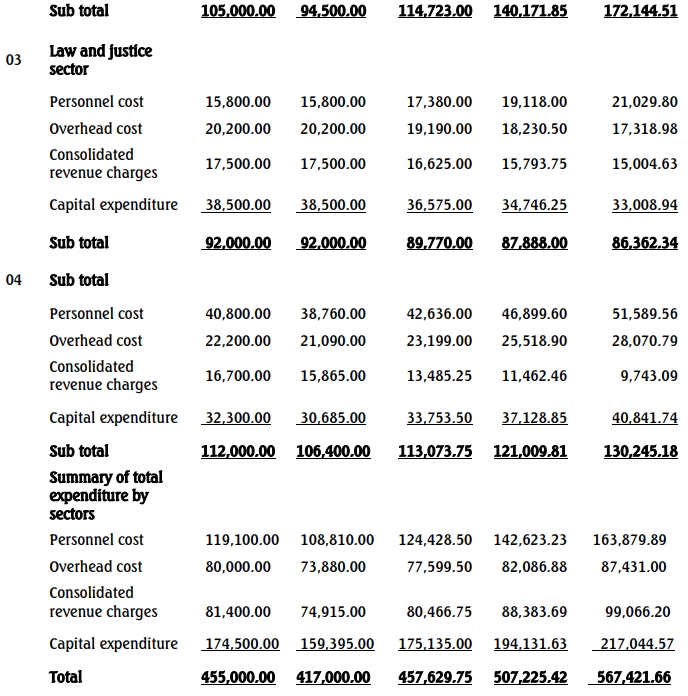

a. Proposed Budget Estimates (2021-2023)

b. National Chart of Accounts (NCOA) Structure

i. Functional Segment: The functional segment classifies the expenditure and revenue according to the functions of government, for example, administrative, economic, social, and environmental functions.

ii. Programme Segment: This segment provides a detailed breakdown of government programmes and sub-programmes within each function. It facilitates the tracking of specific programme performance within the national budget.

iii. Geographical Segment: This segment identifies the location (geographical areas) where expenditures and revenues are generated or allocated. This helps in understanding the impact of government activities across different regions.

c. Steps Required for Budgeting with the National Chart of Accounts

- Identifying the relevant segments (functional, programme, geographical) in line with the national budget priorities.

- Assigning expenditures and revenues to the respective segments based on budget guidelines.

- Compiling the segment-wise data into the government’s overall financial reporting framework.

- Verifying and reconciling the segment data to ensure accuracy and completeness in the budget presentation.