Question

Sekiri Nigeria Limited is a major competitor to Ijor Ventures Limited. Both companies operate in the same industry over the last 20 years.

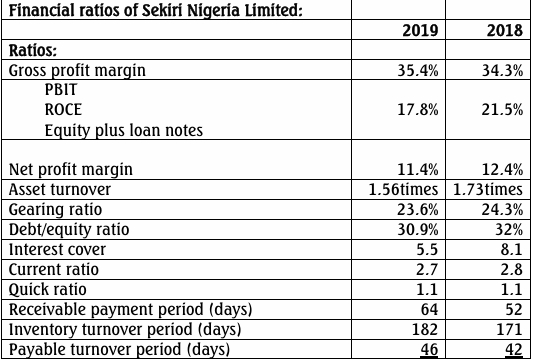

The summarised financial information of Sekiri Nigeria Limited for the last 2 years is as follows:

Summarised Profit or Loss for the Year Ended September 30:

| Description | 2019 (N’m) | 2018 (N’m) |

|---|---|---|

| Revenue | 4,565 | 4,905 |

| Cost of Sales | (2,950) | (3,225) |

| Gross Profit | 1,615 | 1,680 |

| Selling, Distribution & Admin Expenses | (1,095) | (1,070) |

| Interest Expense | (95) | (75) |

| Net Profit Before Taxation | 425 | 535 |

| Taxation | (225) | (260) |

| Profit for the Year | 200 | 275 |

Statement of Financial Position as at September 30:

| Description | 2019 (N’m) | 2018 (N’m) |

|---|---|---|

| Non-Current Assets: | ||

| Intangible Assets | 240 | 200 |

| Tangible Assets (Carrying Amount) | 1,080 | 1,030 |

| Total Non-Current Assets | 1,320 | 1,230 |

| Current Assets: | ||

| Inventories | 1,470 | 1,515 |

| Trade Receivables | 800 | 705 |

| Bank | 260 | 290 |

| Total Current Assets | 3,850 | 3,740 |

| Total Assets | 5,170 | 4,970 |

Equity & Liabilities:

| Description | 2019 (N’m) | 2018 (N’m) |

|---|---|---|

| Equity | ||

| Ordinary Share Capital | 500 | 500 |

| Retained Earnings | 1,730 | 1,650 |

| Total Equity | 2,230 | 2,150 |

| Non-Current Liabilities | 690 | 690 |

| Current Liabilities: | ||

| Trade Payables | 375 | 375 |

| Other Payables | 555 | 525 |

| Total Liabilities | 3,850 | 3,740 |

Sekiri Nigeria Limited declared dividend of N120m each in years 2018 and 2019

Required:

(a) As the Chief Accountant of Ijor Ventures Limited, write a report to your company’s Finance Director analyzing the performance of Sekiri Nigeria Limited.

(10 Marks)

(b) Highlight FIVE areas that will require further investigation, including reference to other pieces of information that would complement your analysis of the performance of Sekiri Nigeria Limited.

(10 Marks)