Question

Answer

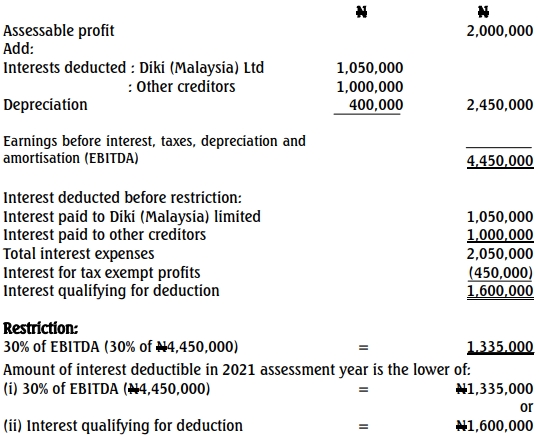

a. XYZ Limited

Computation of interest deductible in 2021 assessment year

The interest deductible is N1,335,000

Treatment of excess interest not deducted in the relevant assessment year

The excess interest of N1,600,000 less N1,335,000 which is N265,000, will be

carried forward and added to the interest expense for that year with a view to

computing its restriction.

It should be noted that the excess interest of N265,000, may only be carried

forward for a period not exceeding five years, that is, 2026 assessment year,

whilst applying for each of the years, the same rule based on which the excess

interest expenditure was first computed.