Question

Answer

Workings

b

(i)

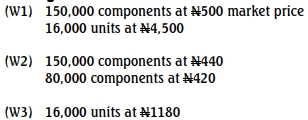

Workings

b

(ii)

(b)(ii) Minimum Price Calculation for New Customer:

- Profit Requirement: N4,500,000

- Remaining production capacity N25,000 = N175,000 – N150,000

- Current Profit: N3,400,000

- Additional Profit Required: N1,100,000

- Contribution per Component: N44 (N1,100,000 / 25,000 components)

- Minimum Price per Component: N484 (N440 + N44)