Question

Answer

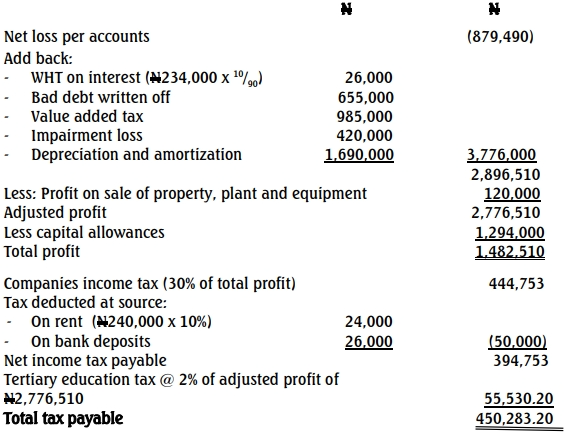

a)

Duru Cobbler Limited

Computation of total profit and taxes payable

For 2019 year of assessment

(b) Zero-Rated Goods and Services under VAT Act:

- Zero-rated goods and services refer to items subject to VAT at 0%. They are taxable but have a 0% rate, allowing input tax recovery.

- Examples of zero-rated transactions include:

- Non-oil exports.

- Goods and services for diplomats.

(c) Penalties for Non-Registration for VAT:

- A penalty of N10,000 for the first month of failure.

- N5,000 for each subsequent month.

- Potential business premises closure.