Question

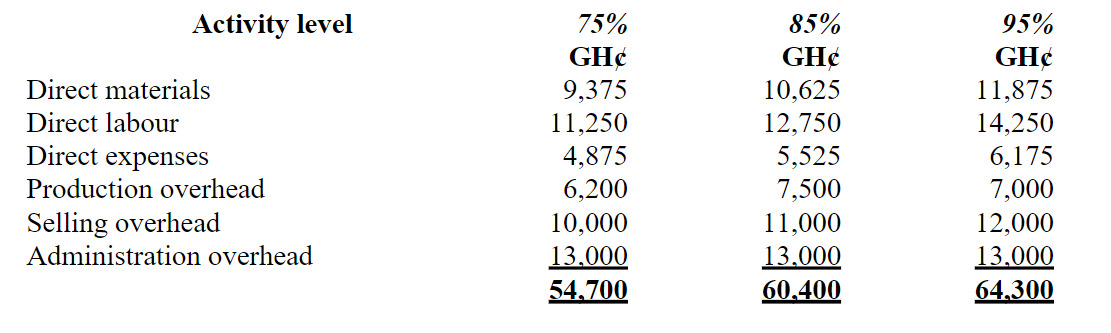

b) The following monthly budgeted cost values have been taken from the budget working papers of MZ Ltd for the year ended 30 September 2019.

During May 2019, actual costs for the activity level of 82% were as follows:

Item GH¢

Direct Materials 10,500

Direct Labour 12,250

Direct Expenses 5,600

Production Overhead 6,250

Selling Overhead 15,150

Administration Overhead 14,200

Total 63,950

Required:

Prepare a budgetary control statement for MZ Ltd on a flexible budget basis for the month of May 2019.

(10 marks)

Answer

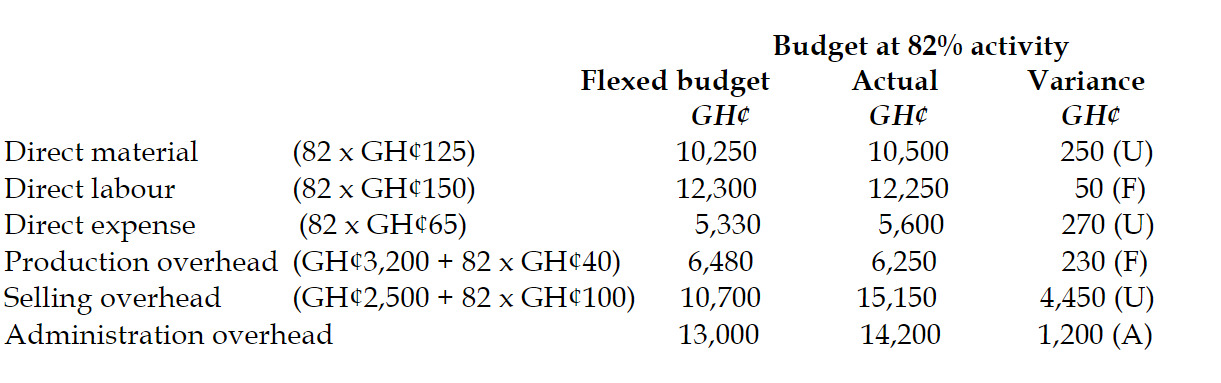

Flexible Budget

Basic calculations

Direct Material

At 75% AL = GH¢9,375/75 = GH¢125; At 85% AL = 10,625/85 = GH¢125; At 95% AL

= GH¢11,875/95 = GH¢125. Thus, direct material cost is variable cost. It is constant at

the unit level but changes with activity level. (0.5 mark)

Direct Labour

At 75% (AL) = GH¢11,250/75 = GH¢150; At 85% AL = 12,750/85 = GH¢150; At 95%

AL = GH¢14,250/95 = GH¢150. Thus, direct labour cost is variable cost. It is constant

at the unit level but changes with activity level.

(0.5 mark)

Direct Expenses

At 75% (AL) = GH¢4,875/75 = GH¢65; At 85% AL = 5,525/85 = GH¢65; At 95% AL =

GH¢6,175/95 = GH¢65. Thus, direct expense cost is variable cost. It is constant at the

unit level but changes with activity level.

(0.5 mark)

Production Overhead

At 75% (AL) = GH¢6,200/75 = GH¢82.67; At 85% AL = 6,600/85 = GH¢77.65; At 95%

AL = GH¢7,000/95 = GH¢73.68. Thus, production overhead is semi-variable cost.

It changes at both total and activity level.

Therefore, using high-low method the separation would be done as follows:

VC/unit = (GH¢7,000 – GH¢6,200)/(95% – 75%) = GH¢800/20 = GH¢40 per 1%

Fixed Cost (Using highest activity level) = 7,000 – (95 x GH¢40) = GH¢3,200 (1 mark)

Selling Overhead

At 75% (AL) = GH¢10,000/75 = GH¢133.33; At 85% AL = 11,000/85 = GH¢129.41; At

95% AL = GH¢12,000/95 = GH¢126.32. Thus, selling overhead cost is a mixed cost. It

changes at both total and activity level.

Therefore, using high-low method the separation would be done as follows:

VC/unit = (GH¢12,000 – GH¢10,000)/(95% – 75%) = GH¢2000/20 = GH¢100 per 1%

Fixed Cost (Using highest activity level) = 12,000 – (95 x GH¢100) = GH¢2,500 (1 mark)

Administration Overhead

This is a fixed cost. It remained constant over all activity level. (0.5 mark)

(Any 18 ticks @ 1/3 = 6 marks)