Question

Answer

i) The variables that determine the value of a real option for BigDaddy Ltd are:

- Exercise Price (Pe): For most real options (e.g., option to expand, option to delay), the capital investment required can be substituted for the exercise price. These options are examples of call options. For an option to abandon, we use the salvage value on abandonment, which is an example of a put option.

- Value of the Underlying Asset (Pa): It is usually the present value (PV) of the future cash flows from the project, excluding any initial investment. For a call option (e.g., option to expand, option to delay), it represents the value of the project being undertaken. For a put option (e.g., option to abandon), it represents the value of the cash flows being foregone.

- Time to Expiry (t): This is the time until the real option expires. In this case, it is the period BigDaddy Ltd can wait before deciding to proceed with the project (2 years).

- Volatility (σ): The volatility of the underlying asset is measured by the uncertainty or standard deviation of future cash flows. Here, the volatility is 25%.

- Risk-free Rate (r): The risk-free interest rate for real options, which reflects the return available from riskless investments, is 5% in this case.

(1 mark for each point, maximum of 5 points)

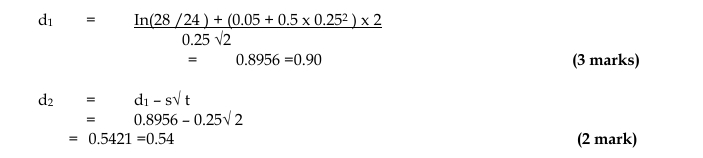

ii) Estimation of the value of the option to delay using the Black-Scholes option pricing model:

Given:

- Current Price (Present Value of the Project): GH¢28 million (GH¢24 million + GH¢4 million NPV)

- Exercise Price (Capital Expenditure): GH¢24 million

- Time to Expiry: 2 years

- Risk-free Rate: 5% per annum

- Volatility: 25%

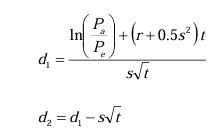

The Black-Scholes formula is as follows:

![]()

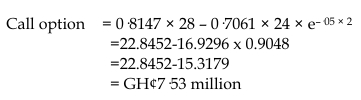

From normal distribution tables:

- N(d2) =0.7054

The project has a value equal to its net present value plus the value of the call option to delay:

TotalValue=GH¢4million(NPV)+GH¢7.53million(optionvalue)=GH¢11.53millionTotal Value = GH¢4 million (NPV) + GH¢7.53 million (option value) = GH¢11.53 million

Comment: This implies that by delaying the decision to start the project, the company can increase the total value of the project by GH¢7.53 million, giving them the flexibility to make a more informed decision once further information about Ebola’s eradication is available. The option to delay is valuable, as it allows the company to mitigate the risk associated with the project’s uncertainty.

(3 marks for calculating d1d1 and d2d2, 2 marks for normal distribution values, 3 marks for calculating option value, 2 marks for the conclusion)