Question

Animal Farm Product Ltd, (AFP), a manufacturer of veterinary medicines for farm animals, wishes to estimate its current cost of capital.

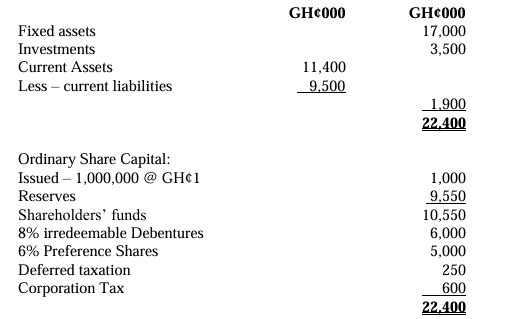

The following figures have been extracted from their most recent accounts:

Other relevant data:

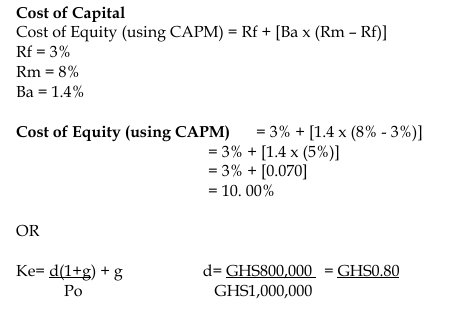

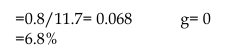

- The current market value of AFP’s ordinary shares is GH¢12.50 per share cum-dividend. AFP’s beta is 1.4, the risk-free rate is 3%, and the return on the SEC index (the market proxy) is 8%. An annual dividend of GH¢800,000 is due for payment shortly.

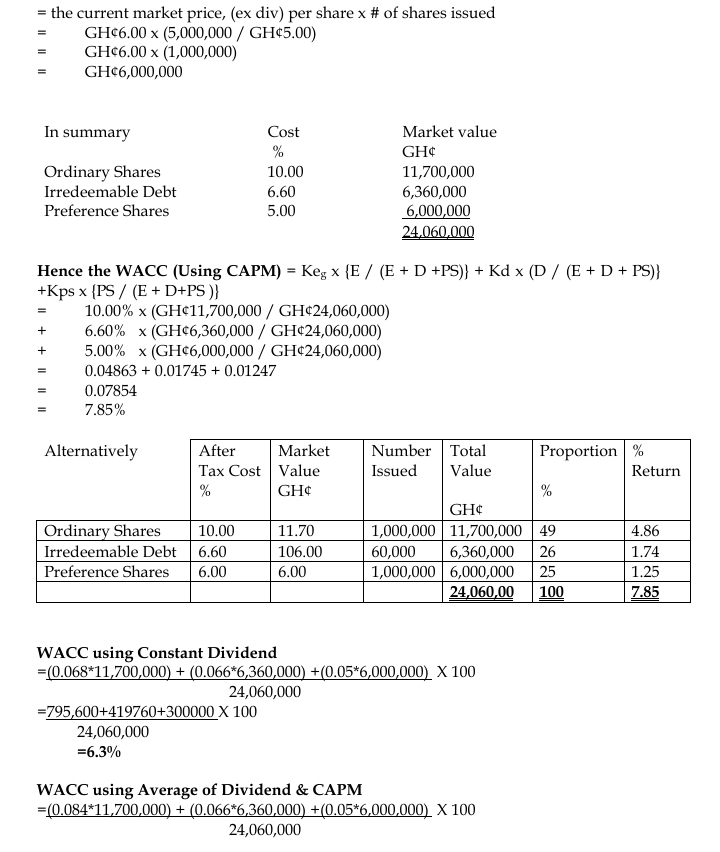

- The 8% debentures are irredeemable and are trading at a current market value of GH¢106.00, a GH¢6.00 premium over their issue price of GH¢100.00. Semi-annual interest of GH¢4 million has just been paid on the debentures.

- The 6% preference shares are trading at a current market value of GH¢6.00, a GH¢1 above their issue price of GH¢5.00. Interest has just been paid on these preference shares.

- There have been no issues or redemptions of ordinary shares or debentures during the past five years, and the corporation tax rate remains at 12.5%. Assume that tax relief on the debenture interest arises at the same time as the interest payment.

Required:

a) Calculate the cost of capital that AFP should use as a discount rate when appraising new marginal investment opportunities. (11 marks)

b) Explain when firms should discount projects using:

- The cost of equity;

- The WACC instead; and

- When should they use neither? You may use the information and your results in part (a) as examples. (6 marks)

c) Discuss what type of covenants might be attached to bonds. (3 marks)

Answer

Cost of Capital Calculation

Cost of Equity (Using CAPM):

Cost of Preference Shares:

- Dividend = 6% of GH¢5 = GH¢0.30

- Market price = GH¢6.00

Cost of Preference Shares=0.30 / 6.00 = 5%

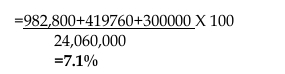

Market Value of Components:

b) When to Use Cost of Equity or WACC:

- Firms should discount projects using cost of equity when they have no debt in their capital structure or when the project being evaluated is very similar to existing equity-financed operations.

- WACC should be used when firms are considering projects that reflect their existing mix of debt and equity financing. In AFP’s case, the WACC of 7.85% is appropriate for evaluating marginal investments.

- Neither cost of equity nor WACC should be used when a firm is considering a project significantly different from its current operations or when the investment would alter the firm’s financial structure.

c) Types of Covenants Attached to Bonds:

- Financial Covenants: These may include restrictions on the company’s financial ratios, such as maintaining a minimum interest coverage ratio or maximum debt-to-equity ratio.

- Asset Covenants: These restrict the disposal of significant assets without bondholder approval.

- Dividend Covenants: These limit dividend payments to ensure that sufficient funds are retained to meet debt obligations.