Question

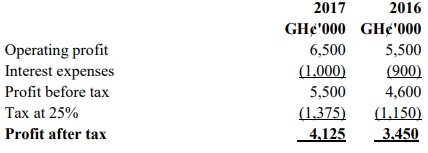

Jabesh Company limited income statements for the years 2016 and 2017 are provided below:

The company directors at a meeting argued that the use of Economic Value Added as a measure of corporate performance is more relevant to current developments in financial markets and agreed to employ it in assessing its performance for years 2017 and 2016.

Additional information is as follows:

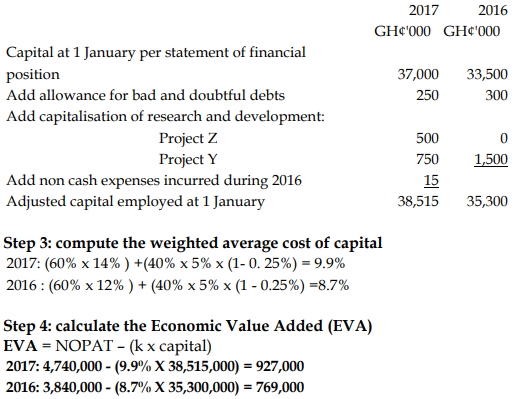

- The allowance for doubtful debts was GH¢300,000 at 1 January 2016, GH¢250,000 at 31 December 2016, and GH¢350,000 at 31 December 2017.

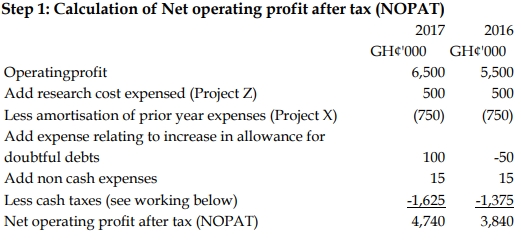

- Research and development costs of GH¢500,000 were incurred during each of the years 2016 and 2017 on Project Z. These costs were expensed in the income statement, as they did not meet the requirements of financial reporting standards for capitalization. Project Z is not complete yet.

- At the end of 2015, the company had completed another research and development project, Project X. Total expenditure on this project had been GH¢1,500,000, none of which had been capitalized in the financial statements. The product developed by Project X went on sale on 1 January 2016, and the product was a great success. The product’s lifecycle was only two years, so no further sales of the product are expected after 31 December 2017.

- The company incurred non-cash expenses of GH¢15,000 in both years.

- Capital employed (equity plus debt) per the statement of financial position was GH¢33,500 at 1 January 2016 and GH¢37,000 at 1 January 2017.

- The pre-tax cost of debt was 5% in each year. The estimated cost of equity was 12% in 2016 and 14% in 2017. The rate of corporate tax was 25% during both years.

- The company’s capital structure was 60% equity and 40% debt.

- There was no provision for deferred tax.

Required:

a) Explain what the directors meant by Economic Value Added (EVA). (2 marks)

b) Calculate the company’s Economic Value Added (EVA) for the years ended 2017 and 2016. (5 marks)

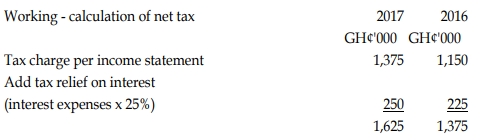

c) Calculate the Net Operating Profit After Tax (NOPAT) for the years ended 2017 and 2016. (6 marks)

d) Explain spin-offs and sell-offs, and identify THREE (3) reasons for spin-offs. (7 marks)

Answer

a) Explanation of Economic Value Added (EVA)

Economic Value Added (EVA) is a performance measure that calculates the true economic profit of a company. It measures the excess of net operating profit after tax (NOPAT) over the company’s cost of capital, which includes both the cost of equity and the cost of debt. EVA is an estimate of the value created by the company above the required return demanded by its capital providers. It is calculated using the formula:

Where WACC is the Weighted Average Cost of Capital, NOPAT is the net operating profit after tax, and capital employed is the sum of equity and long-term debt.

(2 marks)

b) Calculation of EVA for 2017 and 2016

Step 2: calculation of adjusted capital employed at 1 January

c) Calculation of NOPAT for 2017 and 2016

d) Explanation of Spin-offs and Sell-offs

- Spin-off: A spin-off occurs when a parent company creates a new independent company by distributing new shares of a subsidiary or business division. Spin-offs allow the new entity to have a separate management and operations from the parent company, often to unlock hidden value or focus on core operations.

- Sell-off: A sell-off refers to the divestiture or sale of a business unit or subsidiary by the parent company, usually to raise capital or focus on more profitable areas of the business.

Reasons for Spin-offs:

- Better management focus: A spin-off allows a business unit to operate under independent management, which can improve performance as managers focus specifically on the needs of the new entity.

- Unlocking shareholder value: Spin-offs often create value for shareholders by allowing the newly independent company to grow without being constrained by the parent company.

- Tailoring to investor preferences: Investors may prefer different risk profiles or growth trajectories, and spin-offs allow investors to choose between different investment opportunities.