Question

Answer

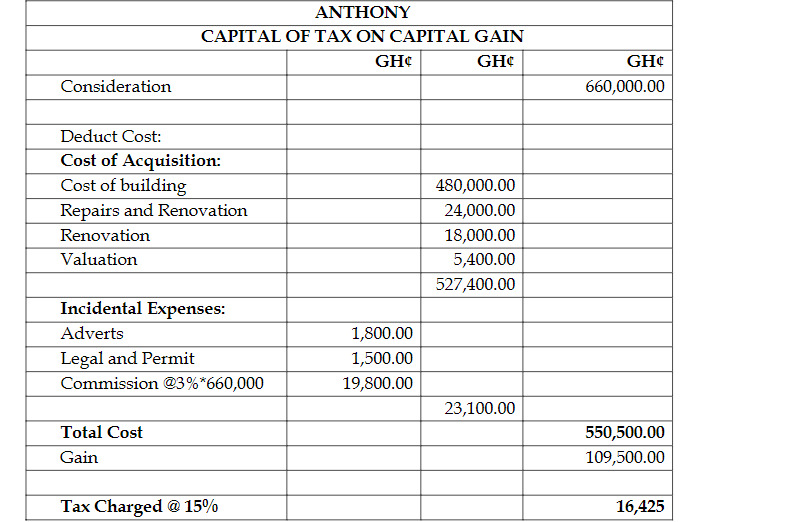

i)

ii) Realisation of Capital Assets: Realisation of capital assets occurs when ownership is transferred through various means such as:

- Sale

- Exchange

- Destruction

- Loss

- Surrender

- Transfer

- Distribution