Question

Answer

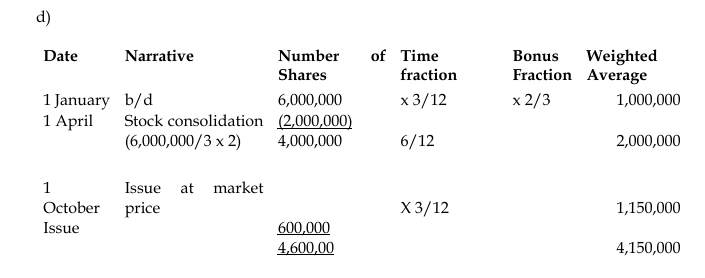

Basic Earnings Per Share (EPS):

- Profit attributable to ordinary shareholders = GH¢(478,000)

- Weighted average number of shares = 4,650,000

- Basic EPS = (GH¢478,000) / 4,150,000 = GH¢11.5 pesewas per share loss.