- 20 Marks

Question

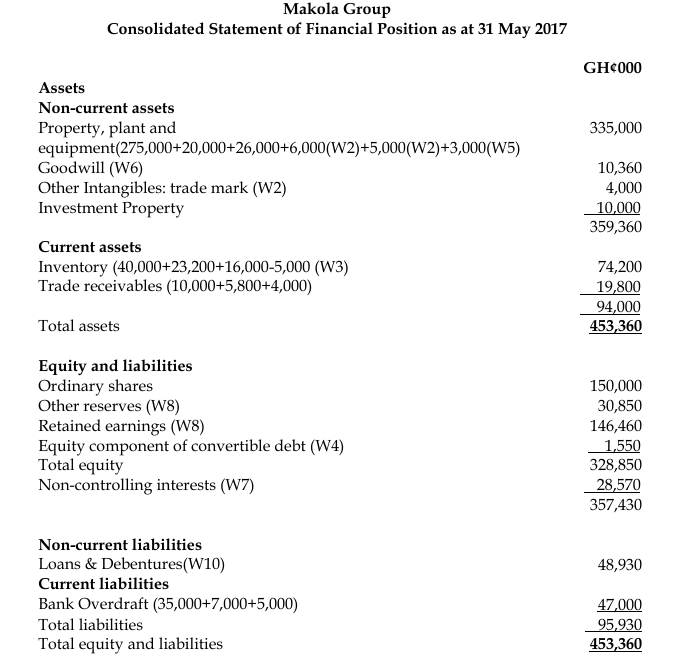

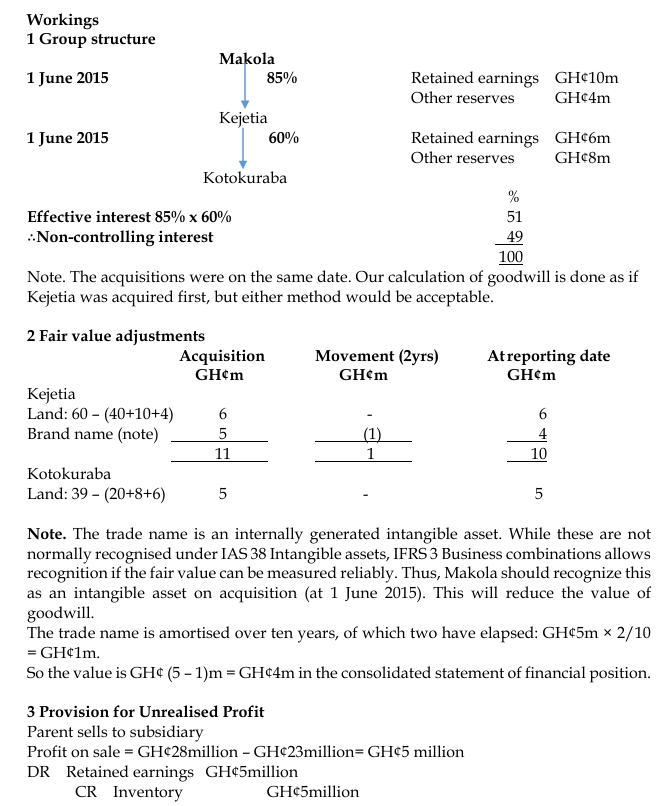

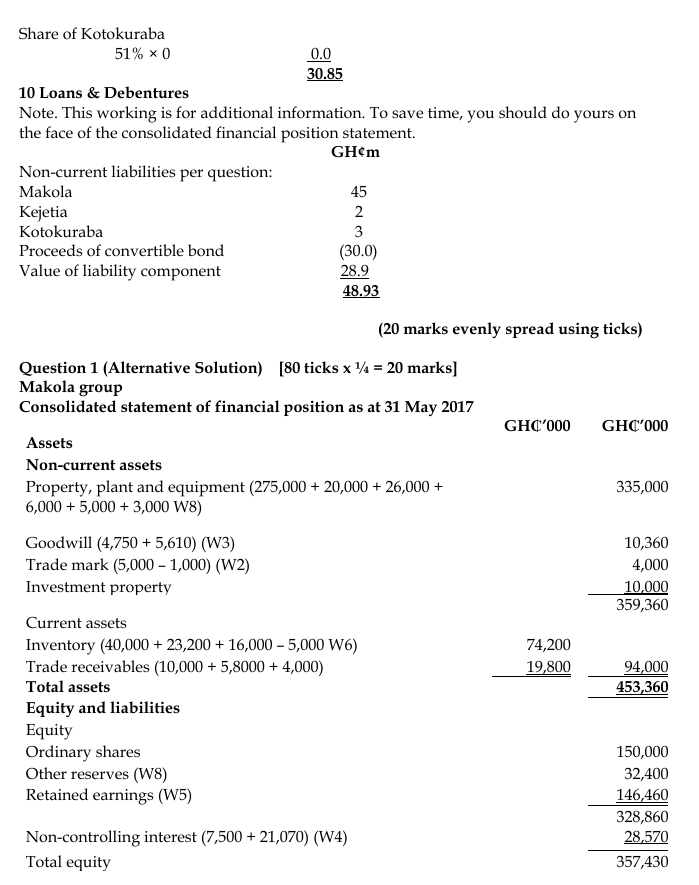

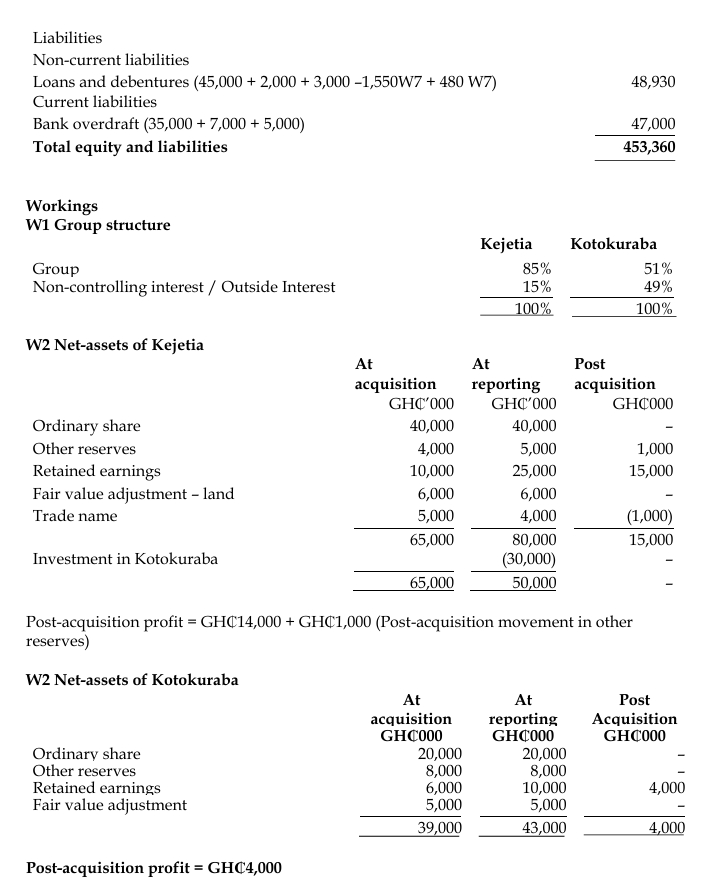

On 1 June 2015, Makola acquired 85% of the ordinary shares of Kejetia when Kejetia’s other reserves were GH¢4 million and retained earnings were GH¢10 million. The fair value of the net assets of Kejetia was GH¢60 million at 1 June 2015. Kejetia acquired 60% of the ordinary shares of Kotokuraba on 1 June 2015 when the other reserves of Kotokuraba were GH¢8 million and retained earnings were GH¢6 million. The fair value of the net assets of Kotokuraba at that date was GH¢39 million. The excess of the fair value over the net assets of Kejetia and Kotokuraba is due to an increase in the value of non-depreciable land of the companies.

Below are the statements of financial position of the three companies as at 31 May 2017:

| Makola (GH¢000) | Kejetia (GH¢000) | Kotokuraba (GH¢000) | |

|---|---|---|---|

| Assets | |||

| Non-current assets | |||

| Property, Plant & Equipment | 275,000 | 20,000 | 26,000 |

| Investment in Kejetia | 60,000 | – | – |

| Investment in Kotokuraba | – | 30,000 | – |

| Investment Property | 10,000 | – | – |

| Current Assets | |||

| Inventory | 40,000 | 23,200 | 16,000 |

| Trade Receivables | 10,000 | 5,800 | 4,000 |

| Total Assets | 395,000 | 79,000 | 46,000 |

| Equity and Liabilities | |||

| Ordinary shares | 150,000 | 40,000 | 20,000 |

| Other reserves | 30,000 | 5,000 | 8,000 |

| Retained earnings | 135,000 | 25,000 | 10,000 |

| Total Equity | 315,000 | 70,000 | 38,000 |

| Non-current liabilities | 45,000 | 2,000 | 3,000 |

| Bank Overdraft | 35,000 | 7,000 | 5,000 |

| Total Liabilities | 80,000 | 9,000 | 8,000 |

| Total Equity and Liabilities | 395,000 | 79,000 | 46,000 |

The following information is relevant to the preparation of the group financial statements:

- There have been no issues of ordinary shares in the group since 1 June 2015.

- Kejetia owns several trade names highly regarded in the market. None have been acquired externally. Makola recognized a GH¢5 million valuation of these trade names in the acquisition, not included in the net assets of Kejetia. Group policy is to amortize intangible assets over 10 years.

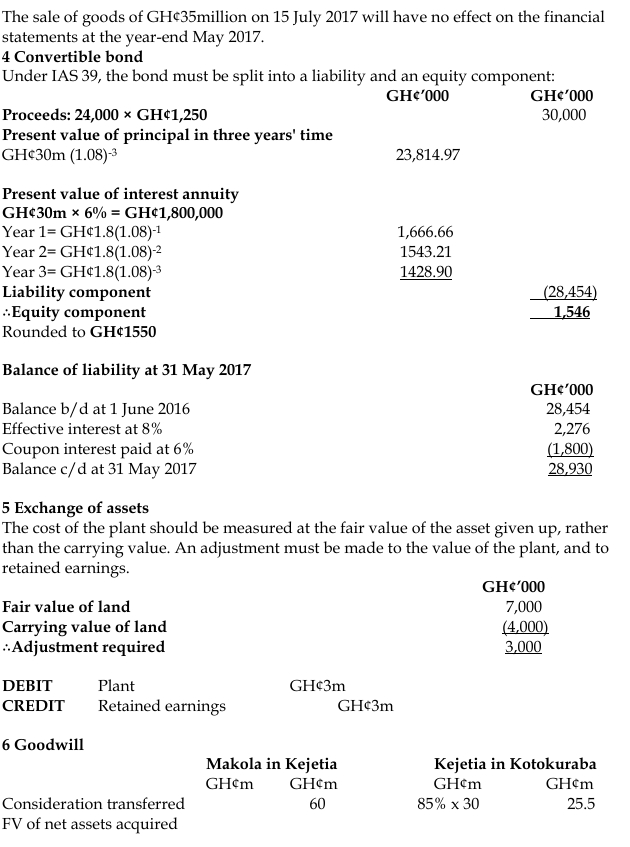

- On 1 June 2016, Makola sold inventory to Kejetia for GH¢28 million (cost: GH¢23 million). Kejetia sold this inventory for GH¢35 million on 15 July 2017.

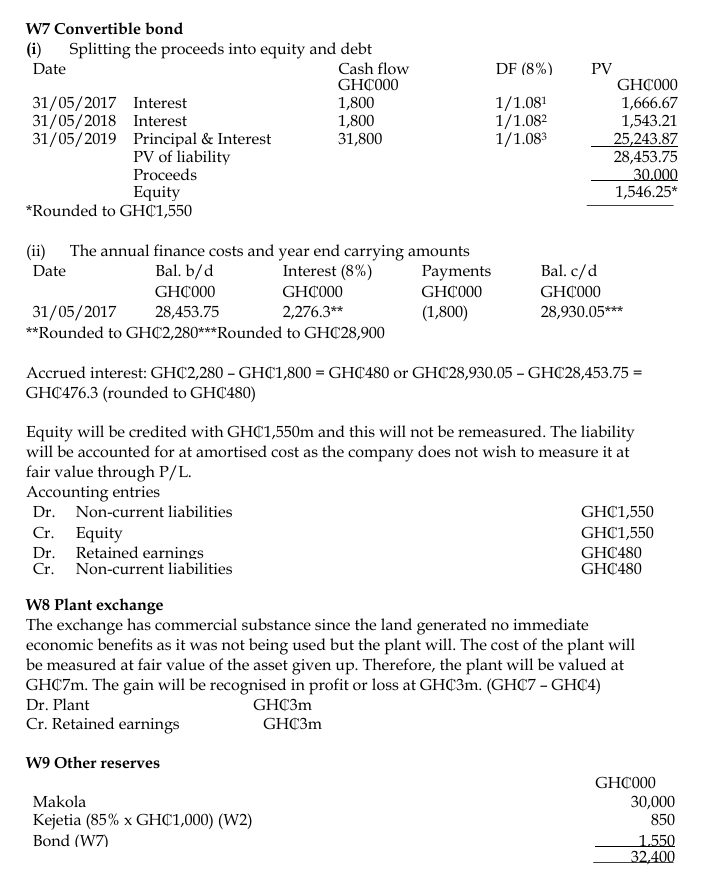

- Makola issued 24,000 convertible bonds with a nominal interest rate of 6% and a three-year term, repayable at par. Interest is payable annually in arrears, and each bond can be converted into 300 shares of Makola. The market interest rate for similar debt was 8%. The bonds were issued on 1 June 2016 and accounted for in non-current liabilities at face value.

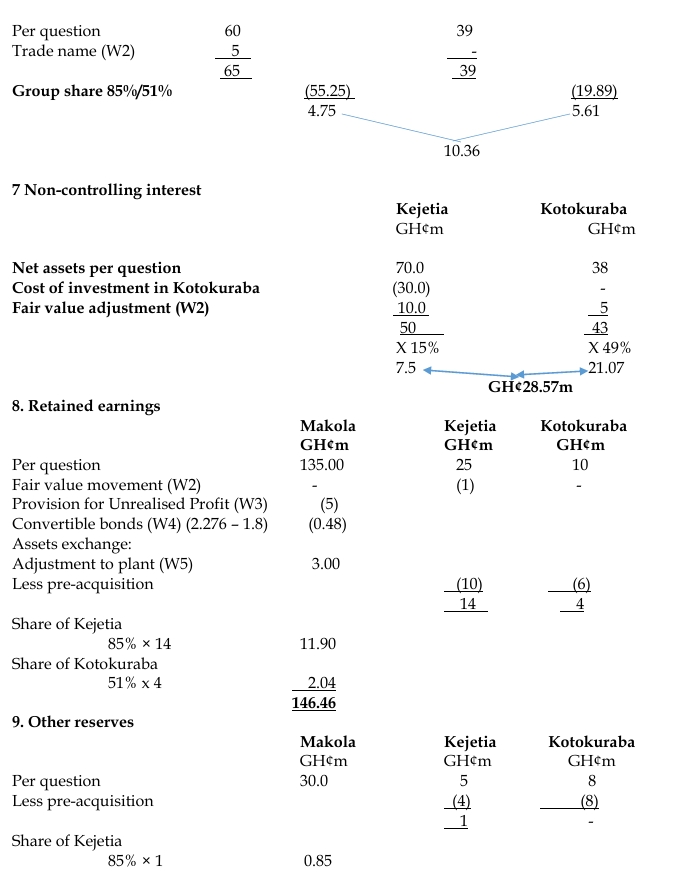

- On 31 May 2017, Makola acquired plant worth GH¢6 million in exchange for land valued at GH¢7 million (carrying value GH¢4 million). Makola made a transfer of GH¢4 million in respect of this transaction.

- Goodwill has been tested for impairment at 31 May 2016 and 31 May 2017, and no impairment loss occurred. The group values non-controlling interest at its proportionate share of the subsidiary’s identifiable net assets at acquisition.

Required: Prepare the consolidated statement of financial position of the Makola Group as at 31 May 2017 in accordance with International Financial Reporting Standards (IFRS).

Answer

- Level: Level 3

- Topic: Consolidated Financial Statements

- Series: NOV 2017

- Uploader: Dotse