- 20 Marks

Question

Below are statements of financial position of three companies: Abuakwa, Tanoso, and Kwadaso as at 31 December 2021:

Statements of Financial Position as at 31 December 2021

| Abuakwa (GH¢ million) | Tanoso (GH¢ million) | Kwadaso (GH¢ million) | |

|---|---|---|---|

| Non-current assets | |||

| Tangible assets | 358.0 | 169.5 | 120.0 |

| Investments | 170.0 | 6.5 | – |

| Total Non-current assets | 528.0 | 176.0 | 120.0 |

| Current assets | 264.0 | 172.0 | 116.0 |

| Total assets | 792.0 | 348.0 | 236.0 |

Equity and Liabilities

| Abuakwa (GH¢ million) | Tanoso (GH¢ million) | Kwadaso (GH¢ million) | |

|---|---|---|---|

| Equity | |||

| Share capital – Ordinary shares (GH¢2 each) | 180.0 | 50.0 | 30.0 |

| Preference shares (GH¢2 each) | – | 40.0 | 13.0 |

| Retained earnings | 330.0 | 66.0 | 56.0 |

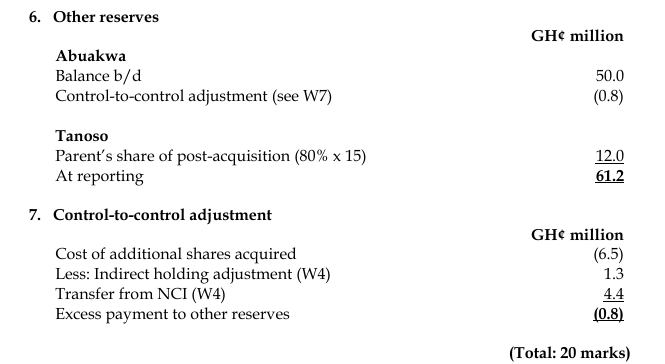

| Other reserves | 50.0 | 23.0 | 8.0 |

| Total equity | 560.0 | 179.0 | 107.0 |

| Current liabilities | 232.0 | 169.0 | 129.0 |

| Total equity and liabilities | 792.0 | 348.0 | 236.0 |

Additional Information:

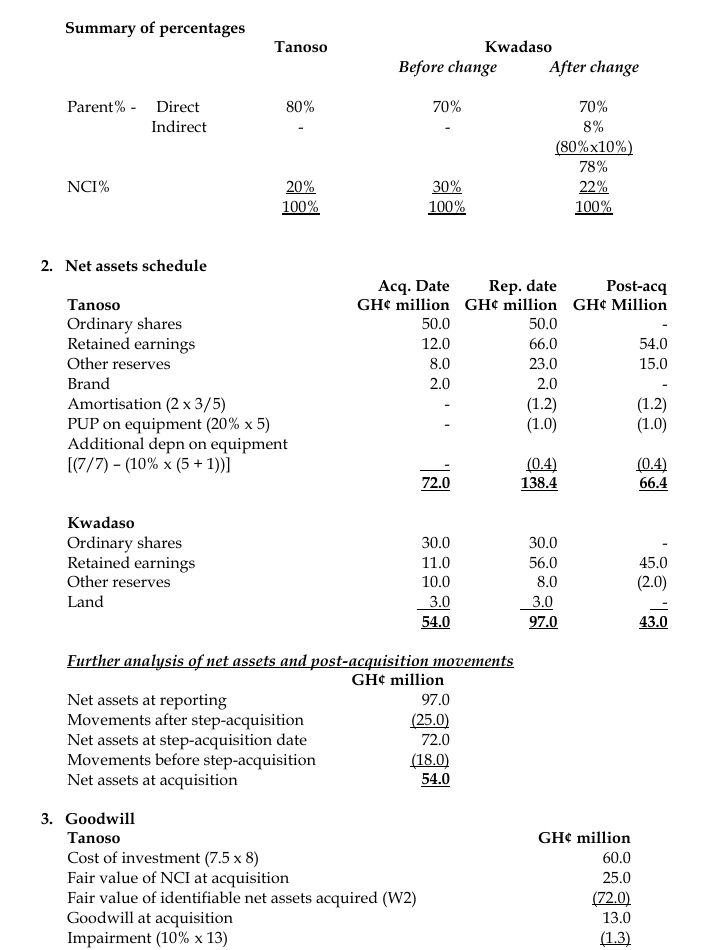

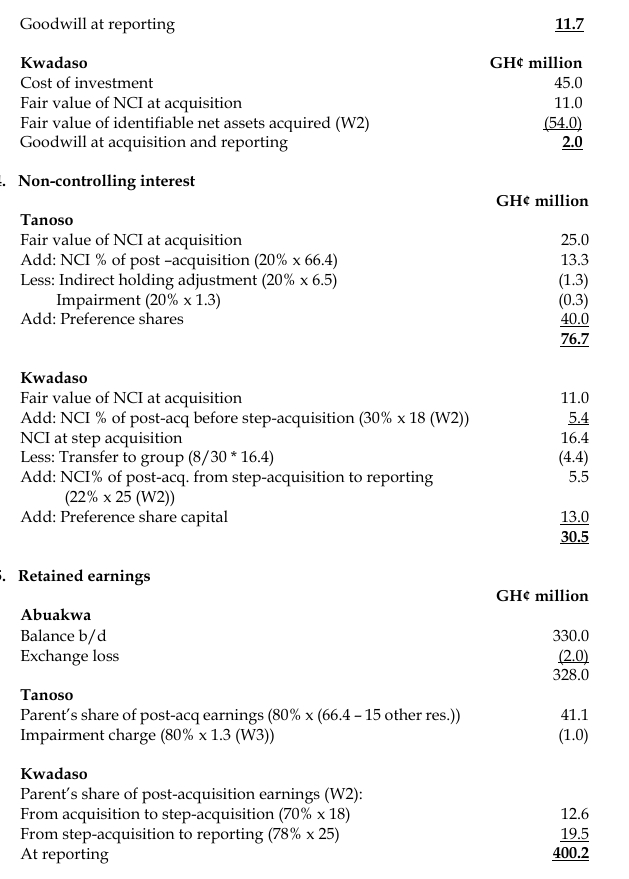

- Abuakwa acquired 20 million shares in Tanoso on 1 January 2019. The consideration, which has been correctly accounted for, was settled by Abuakwa issuing its own ordinary shares of 7.5 million. The fair value of non-controlling interest of Tanoso at the date of acquisition was GH¢25 million.

- The brand name of Tanoso had a fair value of GH¢2 million with a useful life of 5 years. At 31 December 2021, the brand’s recoverable amount was GH¢1.1 million.

- Abuakwa acquired 10.5 million shares in Kwadaso on 31 December 2019. Abuakwa satisfied this consideration by deferring cash payment for a year.

- Kwadaso’s net assets were uplifted by GH¢3 million on a non-depreciable land.

- Tanoso acquired 1.5 million shares of Kwadaso for immediate cash consideration of GH¢6.5 million.

- On 1 January 2021, Tanoso sold machinery to Abuakwa at a 20% profit on cost. Abuakwa depreciates this type of machinery at 10% per annum.

- Goodwill in Tanoso was impaired by 10%.

- Trade payables in Abuakwa include GH¢7 million due to foreign suppliers, with an unaccounted exchange loss of GH¢2 million.

Required:

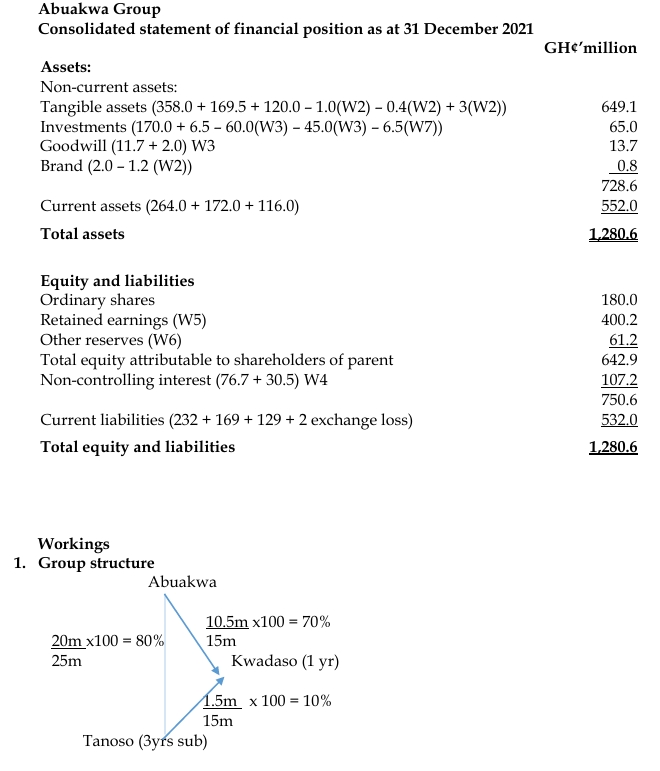

Prepare the consolidated statement of financial position as at 31 December 2021 for the Abuakwa Group. (All figures should be stated in nearest GH¢0.1 million).

Answer

- Topic: Consolidated Financial Statements

- Series: MAR 2023

- Uploader: Dotse