Question

Partey Ltd (Partey) produces flour and various soup powders, and the company is considered as a priority company. On 1 January 2019, Partey owned two refineries in Accra (Weija and Mamprobi) and a refinery in Takoradi. Each refinery comprises building, plant and equipment and a warehouse, all of which were owned by Partey.

Partey has been having financial difficulties and, on 1 February 2019, engaged the services of a business consultant to recommend a survival plan for the company. Unfortunately, staff morale was very low when the business consultant was engaged because their salaries were six months in arrears.

The business consultant’s recommendations were agreed and implemented in the year ended 31 December 2019 as follows:

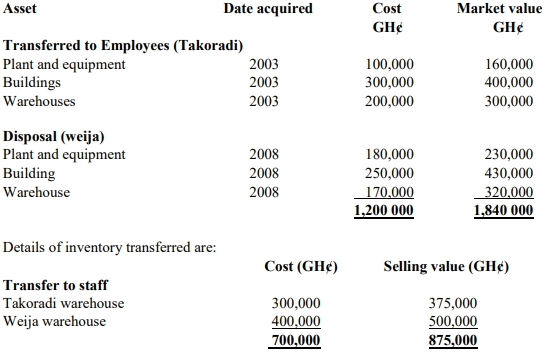

i) The Takoradi refinery was transferred to the employees at market value to be operated as independent business ventures. The inventory in the warehouse was included in the transfer.

ii) The Weija refinery was disposed off, together with all its related fixed assets, to fund Partey’s future business operations and pay off part of the arrears of salaries due to the employees. The employees at this refinery were all reassigned elsewhere. The inventory at the warehouse, valued at cost, was given to the employees as final settlement of their salaries in arrears.

Both the disposal of the Weija refinery and the transfer of the Takoradi refinery to their employees were made on 30 March 2019.

Details of the fixed assets disposed and transferred are:

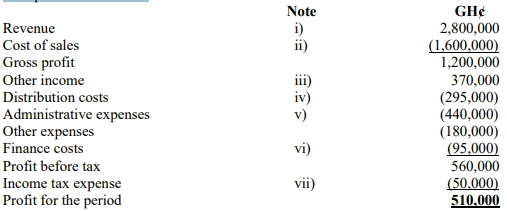

Partey’s statement of profit or loss for the year ended 31 December 2019 in respect of

Mamprobi is as follows:

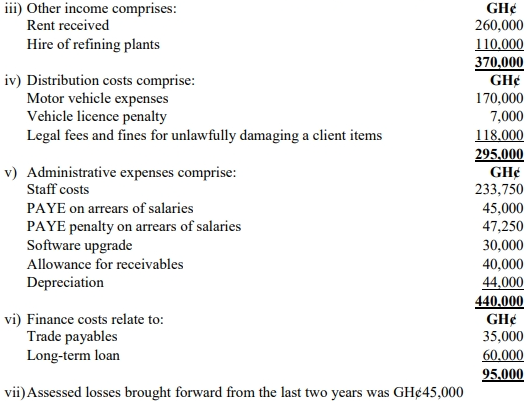

Notes:

i) This amount represents Partey’s ordinary sales for the year.

ii) Included in the cost of sales is the total value of inventory at cost transferred to the

employees (in accordance with the business consultant’s recommendations) on 30 March

2019. No other adjustments were recorded regarding this inventory transfer.

Required:

a) Outline the tax consequences for Partey due to the transfer of the fixed assets and inventory to the employees on 30 March 2019, stating when any taxes should be paid. (4 marks)

b) Assess the tax implications:

i) When the proceeds from the realisation of depreciable assets exceed the written down values? (1.5 marks)

ii) When the proceeds from the realisation of depreciable assets are less than the written down values? (1.5 marks)

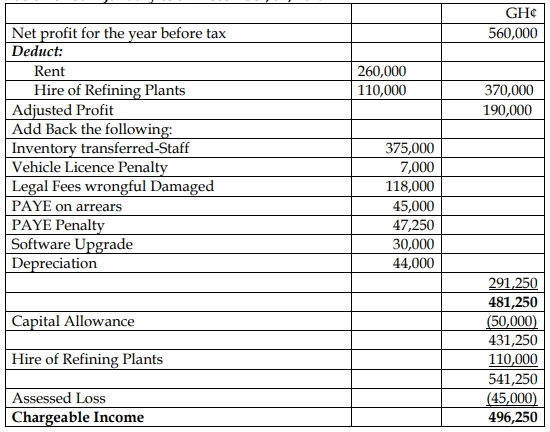

c) Calculate the taxable income of Partey for the year ended 31 December 2019. (8 marks)

d) Explain how shareholders of a company are taxed? (5 marks)

Answer

a) Tax consequences with respect to transfer of assets The transfer of the fixed assets and the stock will be treated as deemed sold Partey Ltd is obliged to account for the gains on the realisation of the assets on transfer. The gains on the realisation should be added to the income of Partey limited Partey Ltd would also account for the VAT on the transferred trading stock, where applicable. The transaction should be included in Partey’s VAT returns for the month of transfer and the VAT paid to the Ghana Revenue Authority by the last working day of the following month. The deemed sale of the stock should also be included in Partey Ltd’s gross income for the year.

b) Gains from realisation of assets

i) When the proceeds from the realisation of depreciable assets exceed the written down value constitutes income in the company’s account.

ii) When the proceeds from realising depreciable assets are less than the written down value, an additional capital allowance shall be granted.

c) Partey Limited Computation of Chargeable Income Year of assessment 2019 Basis Period 1 January to 31 December, 31, 2019

d) Taxation of Shareholders of a Company Where a resident company pays a dividend to a shareholder, the resident company is required to withhold tax on the amount of the dividend paid at the rate of 8%.

A dividend is also deemed to have been paid to each shareholder of a company in proportion to the respective interest of the shareholder, if:

- The dividend consists of profits that are capitalised; or

- Where the Commissioner-General declares part of the company’s income as dividends, where the Commissioner-General is satisfied that a company controlled by not more than five persons and their associates does not distribute to its shareholders as dividends, a reasonable part of the income of the company from all sources for a basis period within a reasonable time after the end of the basis period, the Commissioner-General may, by notice in writing treat as dividend, that part of the income of that company which the Commissioner-General determines to be dividend paid to its shareholders during that period or any other period.