Question

Answer

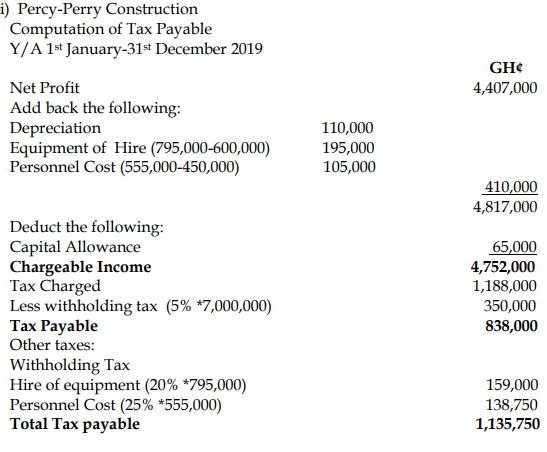

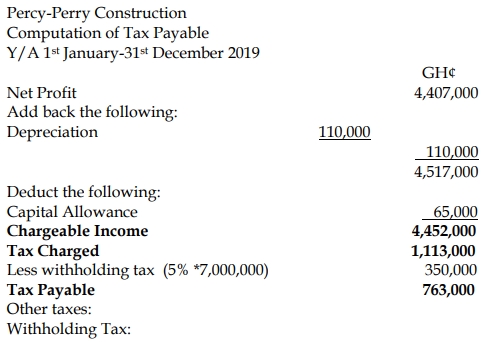

i) Tax Computation for Percy-Perry Construction Ghana Ltd:

Alternative Solution

Commentary on the Treatment of Transactions:

- Equipment Hire from Parent Company:

The equipment hire cost of GH¢795,000 charged by the parent company is higher than the market rate of GH¢600,000. This excess cost of GH¢195,000 is considered non-deductible for tax purposes under transfer pricing regulations and has been added back to the taxable income. - Technical Personnel Cost:

The technical personnel cost of GH¢555,000 charged by the parent company exceeds the local hiring cost of GH¢450,000. The excess cost of GH¢105,000 is also considered non-deductible for tax purposes and has been added back to the taxable income.

ii) Tax Computation for Percy-Perry Engineering Company (USA) Ltd:

| Description | Amount (GH¢) |

|---|---|

| Profit (9,000,000 – 7,000,000) | 2,000,000 |

| Tax @ 25% | 500,000 |

| Less: Withholding Tax (5% of 9,000,000) | (450,000) |

| Tax Payable | 50,000 |

Note: Percy-Perry Engineering Company (USA) Ltd is liable to a 25% tax on the profit attributable to the contract. However, withholding tax deducted on the contract fees paid to the parent company can be used as a credit to reduce the final tax liability.

iii) Objectives of the Ghana Investment Promotion Centre (GIPC):

The GIPC is a government agency tasked with promoting and facilitating investments in Ghana. The key objectives of GIPC include:

- Promoting Investment:

GIPC seeks to attract and promote both local and foreign investments by showcasing Ghana’s investment opportunities and creating a favorable environment for investors. - Setting Guidelines for Foreign Investors:

The GIPC establishes clear guidelines on what foreign investors can do in Ghana, ensuring that foreign participation complements local interests. - Providing Investment Incentives:

GIPC offers various incentives, such as tax holidays and exemptions, to businesses that register with them, especially those in priority sectors such as agriculture, manufacturing, and infrastructure development.