Question

Answer

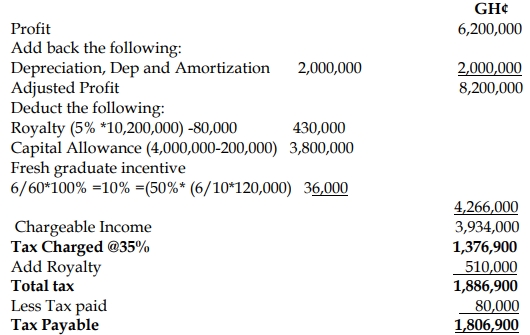

i) Computation of Tax Payable by Kaka Ltd for the 2019 Year of Assessment:

Given that there is no information about the number of times capital allowance has been granted on the written down value, any assumption is correct as capital allowance in mining is granted 5 years straight line methods

ii) Tax Implication of Proposed Investment Decision:

Option 1: Add GH¢100,000 to Working Capital:

- The additional income of GH¢10,000 will be classified as business income and will be subject to corporate tax at the mining rate of 35%.

- Tax payable on GH¢10,000 business income:

35%×10,000=

Option 2: Purchase Treasury Bills:

- The interest income of GH¢10,000 from Treasury Bills will be classified as investment income, and the tax rate on such income is 25%.

- Tax payable on GH¢10,000 interest income:

25%×10,000=

Conclusion:

Kaka Ltd should invest in Treasury Bills, as the tax payable on interest income (GH¢2,500) is lower than the tax payable on additional business income (GH¢3,500), resulting in higher after-tax income from the Treasury Bills investment.