Question

Answer

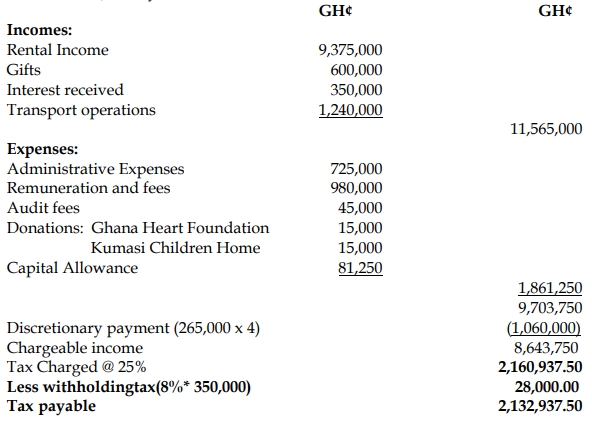

a) Computation of Chargeable Income and Tax Payable by Fenty Trust Ltd for the 2022 Year of Assessment

b) General Tax Rules on Trust Institutions and Trust Beneficiaries

Trust Institutions:

- A trust is taxed as a separate entity from its beneficiaries, with separate calculations required for each trust, regardless of whether they have the same trustees.

- A trust is treated as an entity for tax purposes unless it is a trust of an incapacitated individual (not being a minor), in which case it is taxed as though it were an individual.

- Income and expenses derived or incurred by a trust, or by a trustee (other than as a bare agent), are treated as derived or incurred by the trust and not by any other person.

- Assets owned and liabilities owed by a trust or trustee (other than as a bare agent) are treated as owned or owed by the trust, not by any other person.

Trust Beneficiaries:

- Distributions by a resident trust are exempt from tax in the hands of the beneficiaries.

- Distributions by a non-resident trust are included in the taxable income of the beneficiaries.

- Gains on the disposal of a beneficiary’s interest in a trust are included in the calculation of the beneficiary’s taxable income.