Question

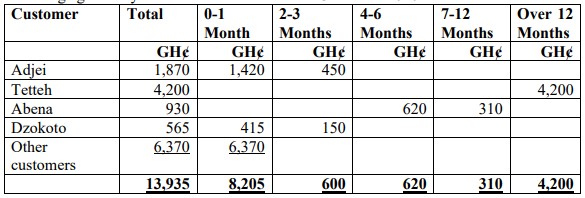

a) Nkrumah runs a small business with total annual sales of GHȼ50,000. He has been reviewing the outstanding balances on his customers’ accounts and has provided the following aged analysis of trade receivables as at 31 March 2020.

Nkrumah’s credit policy is payment within 30 days. The provision for bad debt as at 1 April 2019 was GHȼ880. Nkrumah’s policy for overdue and irrecoverable debts is to:

- Write off as an irrecoverable debt any debt outstanding for over 12 months.

- Create specific provision for any debts outstanding between 4 and 12 months.

- Make no provision for debts up to 1 month old.

- Create a general provision of 4% for all other debts.

Required:

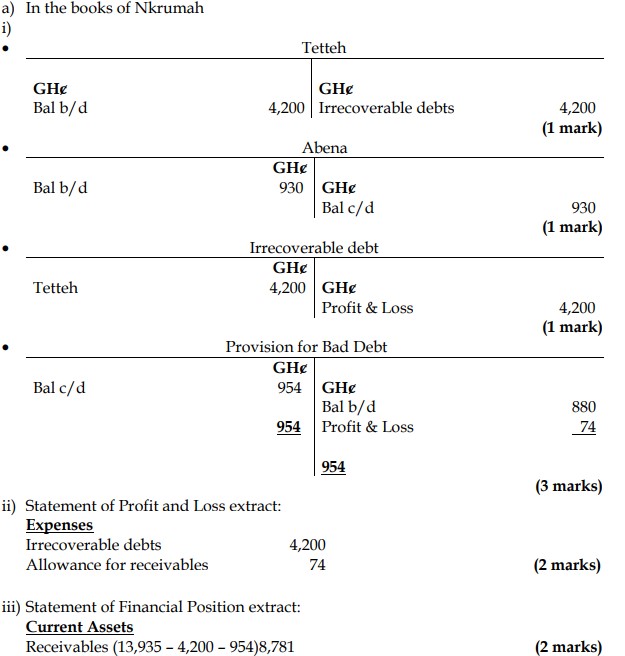

i) Prepare and balance off the following ledger accounts for Nkrumah for the year ended 31 March 2020:

- Tetteh

- Abena

- Irrecoverable Debts

- Provision for Bad Debts

(6 marks)

ii) Prepare the Statement of Profit and Loss extract for irrecoverable debts and provision for bad debts for the year ended 31 March 2020.

(2 marks)

iii) Prepare the Statement of Financial Position extract for receivables as at 31 March 2020.

(2 marks)

b) The admission and retirement of a partner in a firm can only be done if all the existing partners have given consent unless otherwise agreed upon. At the time of admitting or retiring a partner, a new agreement is entered into and the firm is redesigned.

When a partner is admitted or retired in a partnership, some steps (procedures) are followed when accounting for his/her admission or retirement.

Required:

i) Detail the steps required when accounting for admission of a new partner.

(6 marks)

ii) Detail the steps required when accounting for the retirement of a partner.

(4 marks)

Answer

b)

i) Steps Required When Accounting for Admission of a New Partner

- Measure Goodwill:

Calculate the value of goodwill for the old partnership before admitting the new partner. - Recognize Goodwill:

Record the goodwill by crediting the partners’ capital accounts in the old profit-sharing ratio. - Adjust Goodwill in New Partnership:

Eliminate goodwill from the books by debiting the partners’ capital accounts in the new profit-sharing ratio. - Capital Introduction:

Record the capital introduced by the new partner. - Revalue Assets and Liabilities:

Revalue the assets and liabilities to reflect their fair values before the admission of the new partner. - Distribute Accumulated Profits or Reserves:

Allocate any accumulated profits or reserves to the old partners before the new partner is admitted.

(6 marks evenly spread)

ii) Steps Required When Accounting for the Retirement of a Partner

- Measure Goodwill:

Determine the goodwill of the partnership at the time of the partner’s retirement. - Recognize Goodwill:

Allocate the goodwill to the partners’ capital accounts in the old profit-sharing ratio. - Remove Goodwill:

Eliminate goodwill by adjusting the partners’ capital accounts in the new profit-sharing ratio. - Settle Capital:

Pay off the retiring partner’s capital account either in cash or by transferring to a loan account. - Revalue Assets and Liabilities:

Adjust the assets and liabilities to reflect their current values. - Distribute Accumulated Profits or Reserves:

Allocate any reserves or retained earnings to the partners before settling the retiring partner’s account.

(4 marks evenly spread)