- 20 Marks

Question

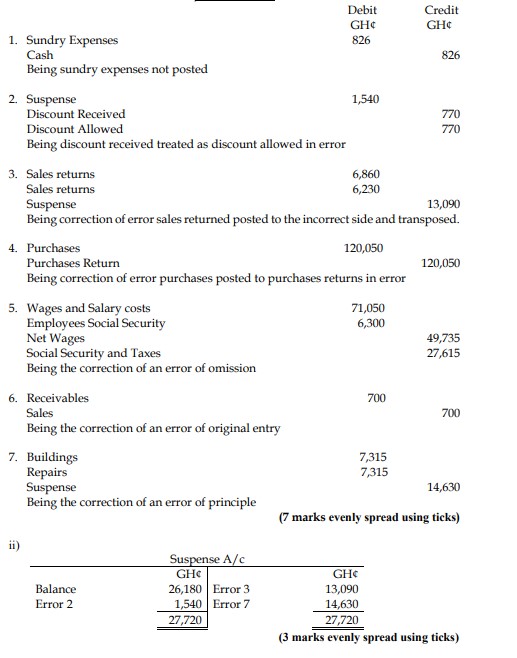

a) K. Avuledor is a sole trader with a small business. The trial balance extracted as at 31 December 2018 failed to agree. The credits exceeded the debits by GH¢26,180. A detailed examination of the books was undertaken, and the following issues were uncovered:

- No entry had been made for expenses paid with cash from the petty cash till. The expenses amounted to GH¢826.

- Discount received of GH¢770 was debited to discounts allowed. The entry in the payables personal account was correct.

- Sales returns of GH¢6,860 were treated correctly in the customer’s account and credited to the sales returns account as GH¢6,230.

- The total in the purchases day book of GH¢120,050 was debited to the purchases returns account.

- The bookkeeper forgot to post the wages and salaries journal for December 2018. No payment has yet been made to employees or the Statutory Authorities. The relevant figures are as follows:

- Wages and salary costs (gross) – GH¢71,050

- Employers Social Security – GH¢6,300

- Employee income taxes (PAYE) – GH¢21,315

- A sales invoice of GH¢7,350 was entered in the sales day book as GH¢6,650.

- A payment for building repairs of GH¢7,315 was credited to both the Buildings account and the cash account.

Required:

i) Prepare journal entries, with appropriate narratives, necessary to correct the above errors.

(7 marks)

ii) Prepare a suspense account to clear the difference.

(3 marks)

iii) Prepare a working schedule showing the effect on the proprietor’s loss in correcting each of the above errors assuming that the loss before these adjustments was GH¢293,090.

(4 marks)

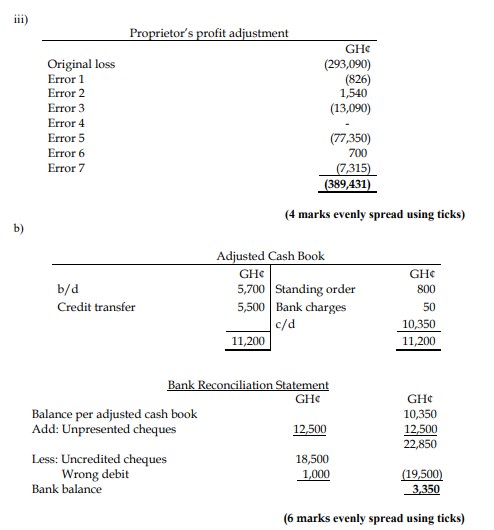

b) The cash book balance of Armah and Co. disclosed a debit balance of GH¢5,700, which did not agree with the closing favorable bank statement balance of GH¢3,350. The following were discovered during the reconciliation:

- Cheques received from customers settling their debts amounting to GH¢18,500 were still in the cashier’s drawer.

- GH¢800 standing order for the payment of electricity charges was paid by the bank. This has not been recorded in the books of Armah and Co.

- Cheque book charge of GH¢50 is yet to be booked by Armah and Co.

- The bank had debited Armah and Co in error of GH¢1,000.

- A credit transfer of GH¢5,500 had been made in favor of Armah and Co. This has not been adjusted in the cash book.

- As at 31 December 2019, cheques totaling GH¢12,500, which were recorded by Armah and Co as paid to suppliers, had not been presented to the bank for payment.

Required:

Prepare an adjusted cash book for Armah and Co and reconcile the adjusted cash book balance with the bank statement balance of GH¢3,350.

(6 marks)

Answer

a) i) Journal Entries

- Tags: Bank Reconciliation, Cash Book, Journal Entries, Profit Adjustment, Suspense account

- Level: Level 1

- Topic: Bank reconciliations, Correction of errors

- Series: NOV 2020

- Uploader: Theophilus