Question

Question:

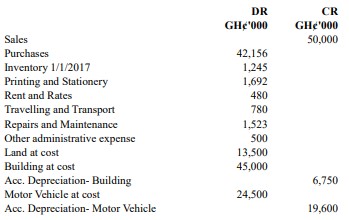

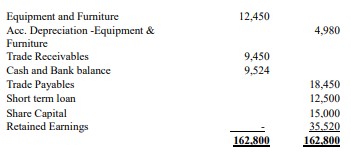

Bob and Sons prepares its financial statements to 31 December every year. At 31 December 2017, the company’s trial balance was as follows:

The following additional information is relevant:

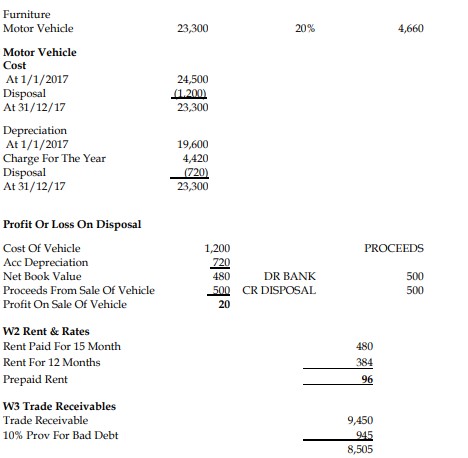

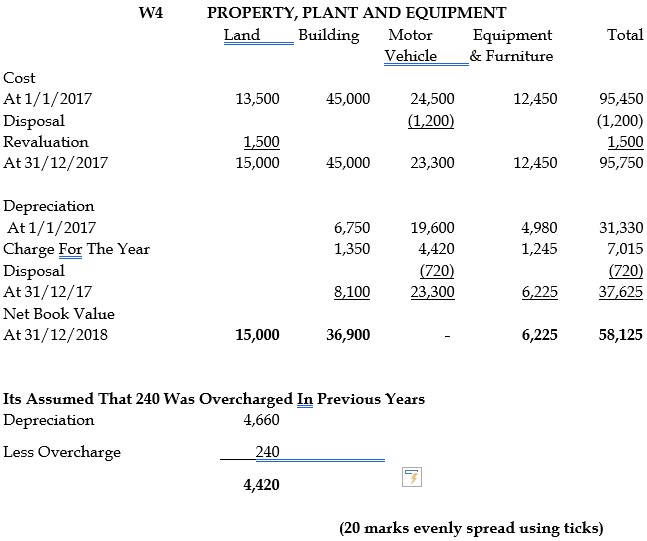

i) Depreciation is to be provided as follows:

- Building – 3% per year on cost

- Motor Vehicle – 20% per year on cost

- Equipment & Furniture – 10% per year on cost

ii) It is the policy of the company not to charge depreciation in the year of disposal.

iii) Land was revalued later in the year for GH¢15,000,000. No change was required to the value of the building.

iv) Inventory value at 31 December 2017 amounted to GH¢1,840,000.

v) Rent recorded in the trial balance represents 15 months rent paid to 31 March 2018.

vi) A provision of 10% of trade receivables is to be made.

vii) During the year, a motor vehicle costing GH¢1,200,000 was disposed of. The vehicle had been in existence for 3 years. Proceeds from the sale of the vehicle were GH¢500,000. This has not been accounted for in the books of Bob and Sons.

Required:

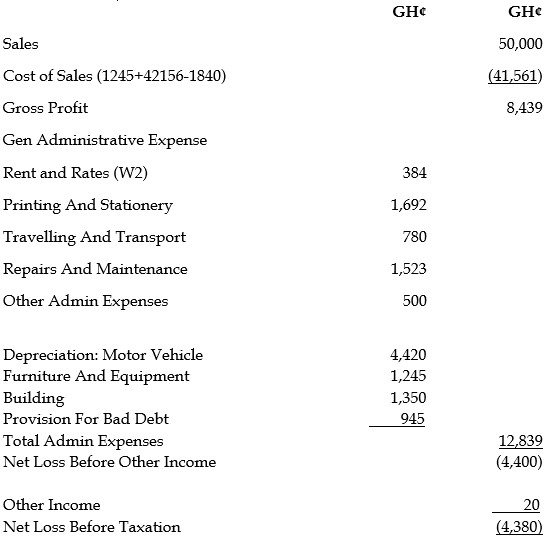

Prepare the Statement of Comprehensive Income for Bob and Sons for the year ended 31 December 2017 and the Statement of Financial Position as at 31 December 2017 in compliance with the provisions of International Financial Reporting Standards (IFRS). (20 marks)

Answer

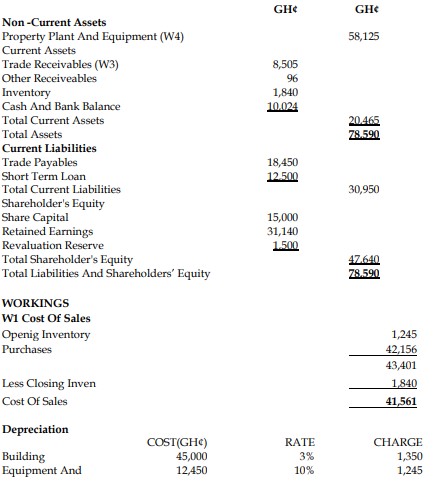

Bob and Sons

Statement of Comprehensive Income for the year ended 31 December 2017

Bob And Sons

Statement Of Financial Position As At 31 December 2017