Question

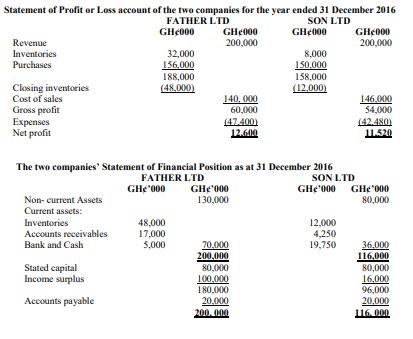

The following is a summary of the Financial Statements of two companies in the retailing business.

Required:

a) Compute the following ratios for both companies:

i) Current Ratio (2 marks)

ii) Acid Test Ratio (2 marks)

iii) Gross Profit Margin (2 marks)

iv) Return on Capital Employed (2 marks)

v) Trade Payable Period (2 marks)

vi) Receivable Collection Period (2 marks)

b) Using the ratios calculated in (a) above, interpret the results under the following categories:

i) Profitability (3 marks)

ii) Liquidity (3 marks)

iii) Efficiency (3 marks)

Answer

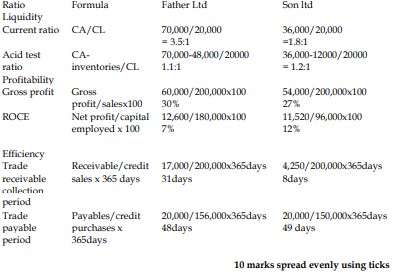

a)

b) Interpretation of Ratios

i) Profitability: Father Ltd has a higher gross profit margin than Son Ltd, indicating better control over cost of sales. However, Son Ltd has a higher ROCE, suggesting better utilization of capital employed.

ii) Liquidity: Both companies can cover their current liabilities with their current assets, but Father Ltd has a better current ratio. However, Son Ltd’s acid test ratio is slightly better, indicating better liquidity when inventory is excluded.

iii) Efficiency: Son Ltd has a shorter receivable collection period, indicating quicker collection of cash from customers. Both companies have similar trade payable periods, showing similar payment cycles to suppliers.