Question

Answer

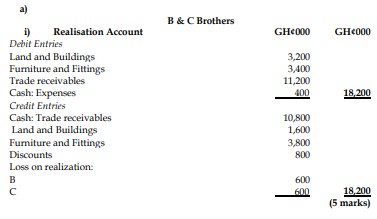

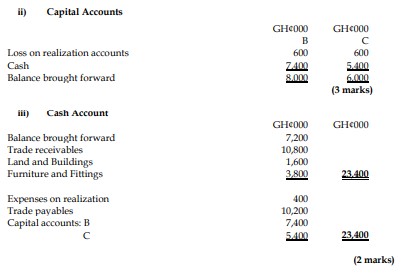

a) i) Realisation Account

b) i) Explain Inventories Inventories, per paragraph 6 of IAS 2, are assets that are:

- Held for sale in the ordinary course of business

- In the process of production for such sale

- In the form of materials or supplies to be consumed in the production process or in the rendering of services.

Inventories per IAS 2 comprise a) Merchandise, b) Production Supplies, c) Materials, d) Work in Progress, e) Finished Goods authorized for issue. (3 marks)

ii) Valuation of Inventories Inventories are measured at the lower of Cost and Net Realizable Value (NRV).

Cost should include all:

- Costs of purchase (including taxes, transport, and handling) net of trade discounts received

- Costs of conversion (including fixed and variable manufacturing overheads)

- Other costs incurred in bringing the inventories to their present location and condition

Net Realizable Value is the estimated selling price in the ordinary course of business, less the estimated cost of completion and the estimated costs necessary to make the sale. (3 marks)

c) Elements of Financial Statement and its recognition criteria Definition of Assets Assets are future economic benefits controlled by the entity as a result of past transactions or other past events.

Criteria for Recognition of Assets:

- It is probable that the future economic benefits embodied in the asset will eventuate; and

- The asset possesses a cost or other value that can be measured reliably.

Definition of Liabilities Liabilities are the future sacrifices of economic benefits that the entity is presently obliged to make to other entities as a result of past transactions or other past events.

Criteria for Recognition of Liabilities:

- It is probable that the future sacrifice of economic benefits will be required; and

- The amount of the liability can be measured reliably.

(Any 2 elements for 4 marks)