Question

Answer

a) In the books of Adom Providers Ltd.

Journal Entries

| Dr (GHȼ) | Cr (GHȼ) | |

|---|---|---|

| Sales | 2,300 | |

| Suspense | 2,300 |

Correction of sales overcast by GHȼ2,300

| Dr (GHȼ) | Cr (GHȼ) | |

|---|---|---|

| Abu | 3,500 | |

| Suspense | 3,500 |

Correction for goods returned and not posted to suppliers account

Suspense: 1,400

Discounts allowed: 1,400

Suspense 1,400

Discounts received 1,400

Correction of discounts totals – discounts received wrongly debited to the discounts allowed account.

Purchases 640

Manu: 640

Correction of a credit purchase not entered in the books

Motor vehicles: 14,000

Motor expenses: 14,000

Correction of error in recording a purchase of a new motor vehicle GHȼ14,000 wrongly recorded as a motor expense.

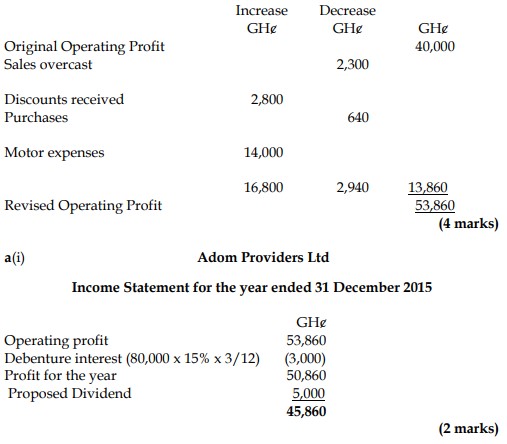

b) Statement to show revised Operating Profit