Question

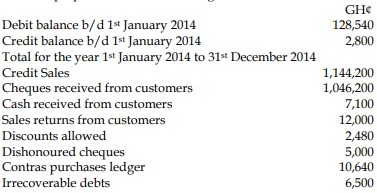

(a) The Sales Ledger Control Account of PC Ltd for the year ended 31st December 2014 has been prepared from the following information:

The Sales Ledger Control Account balance, which is part of the double-entry system, failed to agree with the total receivables of GH¢189,380 as shown by the Schedule of Receivables. The following errors were subsequently discovered:

i) A customer had returned goods to PC Ltd at the selling price of GH¢2,400. The goods had been bought on credit. No entries had been made to record the return of the goods in the accounts of PC Ltd.

ii) The discounts allowed column in the cash book had been overcast by GH¢1,080.

iii) No contra entry had been made in the receivables account in the sales ledger in respect of purchases by PC Ltd of goods at a list price of GH¢2,000. PC Ltd received a trade discount of 10% on these goods. This transaction had been correctly dealt with in the Sales Ledger Control Account.

iv) A credit sale of GH¢3,520 to JT Ltd was correctly recorded in the Sales Ledger Control Account, but no other entry had been made.

v) A cheque received from a customer for GH¢6,900, correctly processed through the books, had subsequently been dishonoured. No entries have yet been made to record this dishonoured cheque.

vi) DT Ltd, a customer, has recently been declared bankrupt and the debt of GH¢3,500 is to be written off, but no entries have yet been made.

Required:

a) Prepare a revised Sales Ledger Control Account for the year ended 31 December 2014. (9 marks)

b) Prepare a statement showing the correct total of the Schedule of Receivables for the year ended 31 December, 2014. (5 marks)

c) Discuss TWO advantages to PC Ltd of using control accounts. (6 marks)

Answer

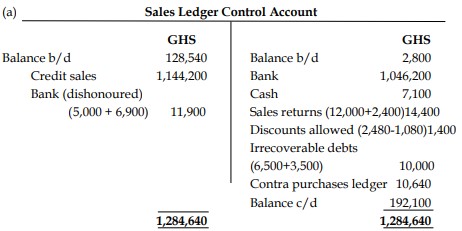

a) PC Ltd

Revised Sales Ledger Control Account for the year ended 31 December 2014

b) PC Ltd

Correct Schedule of Receivables for the year ended 31 December 2014

| Description | GH¢ |

|---|---|

| Original balance | 189,380 |

| Add: Dishonoured cheque | 6,900 |

| Add: Credit sale to JT Ltd | 3,520 |

| Less: Sales returns | (2,400) |

| Less: Contra (2,000 * 90%) | (1,800) |

| Less: Irrecoverable debt | (3,500) |

| Correct Schedule of Receivables | 192,100 |

c) Advantages of Using Control Accounts

- Error Detection: Control accounts provide an independent check on the entries made in the ledger accounts. Discrepancies between the control accounts and the ledger accounts indicate the presence of errors, making them easier to identify and correct.

- Fraud Prevention: By separating duties and allowing senior staff to oversee the control accounts, it becomes harder for fraudulent activities to occur unnoticed, as the control accounts offer an additional layer of oversight.