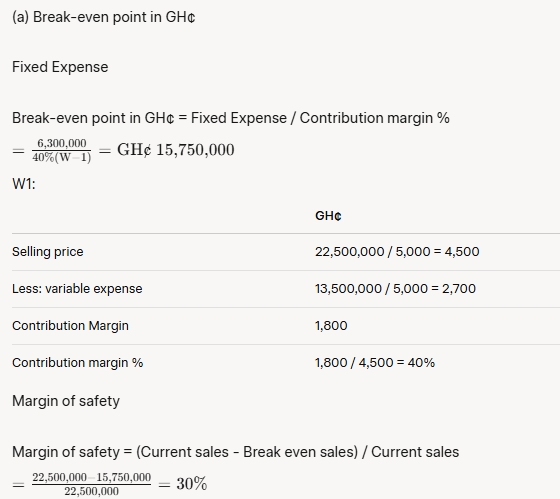

Question

Answer

(b) New CM Ratio

| GH¢ | |

|---|---|

| Selling price | 4,500 |

| Less: variable expense | 2,700 + 600 = 3,300 |

| Contribution Margin | 1,200 |

| Contribution margin % | 1,200 / 4,500 = 26.67% |

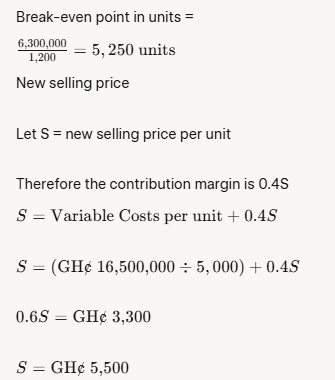

Break-even point in units

(c) No. of units to be sold next year to earn a profit of GH¢3,150,000

Selling price

| GH¢ | |

|---|---|

| Selling price | 4,500 |

| Less: variable expenses | 3,300 × 50% = 1,650 |

| Contribution margin | 2,850 |

Break even point in units = (Fixed Expense + Target Profit) / Contribution margin per unit